Brea Divorce Attorney

Divorce is one of life’s most difficult, challenging, and often sad experiences. For residents of Brea, California, navigating this process can be significantly easier with the right legal support. It’s essential to prepare and thoroughly complete your research before choosing a lawyer to represent you. Compare attorneys, law firms, and their online presence.

What are they saying? What are they not saying? For those in Brea, the choice is clear. If you are thorough in your research, the choice of who to hire of the 600 plus divorce lawyers in Orange County is not difficult.

Minyard Morris has been serving your community since 1977. For over 46 years, we have dedicated ourselves to supporting Brea and Orange County residents in their family law matters. Our team of 20 divorce lawyers boasts nearly 350 years of combined experience, exclusively focusing on family law cases filed in Orange County.

Among our team, 9 are Certified Family Law Specialists, certified by the California State Bar. In 2024, the preeminent independent lawyer rating service BEST LAWYERS IN AMERICA listed 19 of 20 Minyard Morris attorneys.

Our firm’s growth and success stems from our commitment to listening to and hearing our clients, understanding their objectives, and working tirelessly to achieve their goals. We prioritize client service and strive to resolve cases efficiently so our clients can begin the next chapter of their lives at the earliest opportunity.

We aim to find solutions from the very beginning, rather than waiting until the eve of a trial or a hearing.

Our Orange County Family Law Services

We handle a wide range of family law matters for our Brea clients, including:

- Child Custody

- Property Division

- Child Support

- Spousal Support

- Prenuptial Agreements

- Separate Property Characterization

- Breach of Fiduciary Duties/Misappropriation

- Domestic Violence

- Valuation of Separate Business Interests

- High Net Worth Estates

- High Conflict Child Custody Disputes

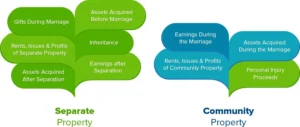

While family law encompasses child custody, domestic violence, and support issues, it primarily involves the division of a marital partnership’s assets. This doesn’t mean each party receives 50% of every asset, but rather that each party receives assets of equal value. One of our main tasks is to make certain that our clients receive at least their fair share of the assets.

Valuing and dividing assets seems simple. Sometimes it is and often it is not, dividing cash, a bank account or a stock account is generally easy. However, in order to arrive at an equal division of an estate that includes, illiquid investments, real estate, businesses, intellectual property, or collectibles, the assets must be valued.

Valuing these assets is often very complex. If your estate has these complexities, you need a divorce lawyer with experience in this area of the law. Minyard Morris has lawyers who handle these types of cases and it has lawyers who handle the normal Orange County divorce at substantially lower hourly rates.

Dedicated Brea Divorce Attorneys

If you are a resident of Brea seeking experienced and dedicated legal representation for your divorce, consider Minyard Morris. Our expertise and commitment to client service can successfully help you navigate this challenging time with confidence. Call 949-724-1111 or use our confidential contact form to arrange your initial consultation.