Minyard Morris, a distinguished family law firm in Orange County, has established itself as a leader in the field through its strategic approach, extensive resources, and commitment to expeditious case resolution. The firm’s unique structure and methodology offer significant advantages in navigating complex matrimonial and family law matters.

Leveraging Firm Resources and Expertise

With a team of 20 divorce lawyers possessing over three and on-half centuries of combined experience, Minyard Morris utilizes its substantial resources to provide comprehensive legal services:

- Diverse Expertise: The firm’s extensive team offers multifaceted perspectives and specialized knowledge across various aspects of family law.

- Collaborative Synergy: Regular strategy sessions ensure that each case benefits from the collective wisdom of the entire firm.

- Comprehensive Case Preparation: The firm’s resources allow for thorough analysis and meticulous preparation of each case.

Strategic Focus and Collaborative Approach

Minyard Morris emphasizes strategic planning through its innovative collaborative model:

- Thrice-Weekly Strategy Sessions: Mandatory meetings held every Monday, Tuesday, and Thursday facilitate in-depth case analysis and strategic brainstorming.

- Collective Intelligence: Clients benefit from the insights of 20 Orange County divorce lawyers, providing a comprehensive approach to case management.

- Tailored Strategies: Each case receives a customized approach based on the client’s specific circumstances and objectives.

Commitment to Expeditious Resolution

A hallmark of Minyard Morris’s practice is its dedication to resolving cases efficiently:

- Proactive Case Management: The firm is renowned for its sense of urgency in addressing client issues.

- Strategic Decision-Making: Divorce lawyers skillfully determine optimal strategies for settlement or litigation.

- Efficient Problem-Solving: The collaborative approach facilitates timely, informed decisions on case strategy.

Client-Centric Service Model

Minyard Morris’s approach is designed to deliver superior client service:

- Personalized Representation: Our Tustin clients are matched with divorce lawyers whose expertise aligns with their specific needs.

- Comprehensive Analysis: The firm provides strategic advice with a thorough evaluation of all options relative to our Tustin clients’ goals.

- Confidentiality and Discretion: A strong commitment to client privacy is maintained throughout the legal process.

Specialized Orange County Expertise

With over 48 years of exclusive focus on Orange County family law, Minyard Morris offers:

- In-Depth Local Knowledge: Extensive understanding of local rules, judicial preferences, and court practices.

- Targeted Expertise: Specialization in both high-net-worth and conventional family law cases.

- Established Reputation: Recognized leadership in the Orange County family law community.

By combining the resources of a large firm with a strategic, urgent approach to case resolution, Minyard Morris provides its Tustin clients with a distinct advantage in family law matters. Their commitment to collaboration, efficiency, and client service sets a new standard in family law practice. This unique approach ensures that clients receive not only expert legal representation but also benefit from a collective effort aimed at achieving optimal outcomes in their cases.

Collaborative Strategy Meetings

These mandatory conferences take place every Monday at 5:00 pm, Tuesday at noon, and Thursday at noon. During these meetings, the lawyers discuss various aspects of pending cases, including:

- Strategies for dealing with opposing counsel

- Approaches to unique issues with assigned judicial officers

- Relevant case law and recent appellate court decisions

- New statutes and seminar insights

- Similar cases handled by the firm’s lawyers

- Settlement options and trial strategies

- Evidentiary issues and probability of prevailing

- Clients’ objectives and goals

Benefits to Our Tustin Clients

The value of these collaborative meetings to clients is significant, though difficult to quantify precisely. By leveraging the collective experience and knowledge of 20 divorce lawyers who specialize in Orange County cases, Minyard Morris offers a distinct advantage over smaller firms. Some key benefits include:

- Rapid access to relevant case law and precedents

- Reality checks on disputed issues

- Insights into the odds of winning particular issues

- Expert recommendations for specific cases

- Creative solutions for settlement roadblocks

Commitment to Excellence

Minyard Morris dedicates substantial resources to these meetings, which are never billed to Tustin clients. The firm views this practice as a crucial differentiator in the family law field, demonstrating their commitment to providing the best client service and achieving optimal results. This collaborative approach not only enhances the quality of legal representation but also attracts talented divorce lawyers to the firm. It’s a testament to Minyard Morris’s dedication to excellence and their unique position in the Orange County family law community.

Tustin Divorce Lawyers for Business Owners: Navigating the Complex World of Divorce with Business Assets

Divorce is rarely a straightforward process, and for business owners, it can add a greater degree of complexity. When a business is part of the marital property, it’s essential to understand how courts approach its valuation and equitable distribution. Unlike simpler assets, the involvement of a business in divorce proceedings introduces additional layers of complexity that call for specialized expertise and careful planning. This article provides an in-depth guide on handling business assets in divorce, offering key insights for Tustin business owners facing this unique challenge.

The goal of this article is to assist you in working more effectively with your divorce lawyers. By learning about business valuation and division, you can become a valuable partner to both your divorce lawyer and any forensic accountant engaged in your case, making the process more efficient, cost-effective, and strategically sound.

Why Hiring Both a Divorce Lawyer and a Forensic Accountant Is Essential

Hiring a divorce lawyer and a forensic accountant may seem like a large expense, but the costs of not retaining these experts could be far greater. The central question to consider is: what financial repercussions might there be if you don’t hire a lawyer and accountant to ensure an accurate business valuation? An incorrect valuation could lead to significant financial losses. Engaging an experienced divorce lawyer in Orange County may turn out to be one of the best financial choices you make in a divorce, especially when you factor in the difference between a professional valuation and an uninformed estimate. Familiarizing yourself with these issues can also help you work more closely with your divorce lawyer and forensic accountant, which may ultimately reduce expenses.

Is an Expert Required for Valuing a Business in Divorce?

While a business owner can technically offer testimony regarding the value of their business, the court often finds this testimony less persuasive, especially if the other party has hired an experienced valuation expert. Business owners typically lack the specific legal knowledge related to valuation issues in family law cases and the rules of evidence that are necessary to present a compelling case. This gap in knowledge could limit their ability to testify effectively or even prevent certain documents from being admitted into evidence.

In contrast, a qualified valuation expert provides a substantiated opinion based on thorough research and analysis. Courts generally place greater trust in the assessment of a qualified expert than in the subjective valuation of a business owner. While a divorce lawyer can collaborate with a forensic expert to build a comprehensive case, the divorce lawyer alone cannot offer a professional business valuation. Without a forensic accountant, a divorce case involving a business lacks the complete team necessary to present a compelling, evidence-backed business valuation. Ultimately, the court will assess which side has presented the more reliable evidence, and it’s highly unlikely that a judge would rely solely on the business owner’s personal opinion.

What Information Must Be Disclosed to Your Spouse About the Business?

As a business owner, you are required by law to provide your spouse with all relevant information regarding the business. Determining what constitutes “relevant” information can be challenging, but a wise approach is to consider, “What would I want to know if I were on the other side of this case?” Over-disclosure is generally recommended to minimize the risk of having your settlement or judgment revisited later. Over-disclosure means providing any documents and information that could impact the valuation of the business. Some advisors suggest that a business owner should disclose any information they would want to know if they were considering purchasing the business. Sharing full details with your divorce lawyer can also help them guide you more effectively throughout the process.

Should You Wait to Be Asked for Documentation or Disclose Voluntarily?

No, waiting for your spouse to request documents is insufficient. California law requires business owners to voluntarily provide all significant information to the other party. This includes both physical documents and verbal information, such as any informal offers to buy the business.

What Are the Consequences of Failing to Disclose Key Business Details?

Failure to disclose material business information can result in serious penalties. Depending on the circumstances, including any intent, motivation, or malice behind the omission, penalties can include awarding the other party 50% to 100% of damages incurred due to the lack of disclosure, as well as significant attorney fees. Full, proactive disclosure is the best way to avoid these risks and to ensure that you are meeting your legal obligations.

Must You Disclose Any Offer Received to Purchase the Business?

Yes, any offer to purchase the business, even if it was only verbal or did not result in a sale, is considered a material fact that must be disclosed. Details regarding the terms, proposed price, and the potential buyer’s identity could be critical in assessing the business’s value in divorce proceedings.

Is Disclosure Required for a Business Appraisal?

Yes, any business appraisal must be disclosed, regardless of the reason it was conducted, the date it was completed, or the valuation methods used. Courts consider past appraisals highly relevant in assessing the business’s current value, even if the appraisals were initially performed outside the divorce context.

Final Declarations of Disclosure: What Are They and Are They Mandatory?

California’s Family Code requires both spouses to exchange Preliminary Declarations of Disclosure, followed by Final Declarations of Disclosure. Preliminary disclosures are mandatory and cannot be waived, while Final Declarations may be waived if both parties consent. However, even if the formal Final Declaration is waived, the obligation to provide fully updated and accurate information remains. In other words, while the document itself can be waived, full transparency regarding the business’s financial status and value is still required.

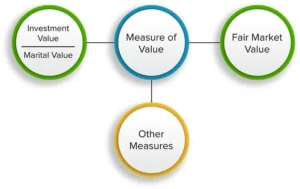

What Is the Investment Value of a Business in a California Divorce Proceeding?

In divorce cases, businesses are not always assessed based on fair market value. Many businesses may not be sellable at a price that reflects their true worth to the owner, yet they can still have significant “investment value.” A common misconception is that a business lacks value if it relies heavily on the spouse who operates it. While some businesses depend on the owner’s involvement, courts in Orange County often calculate the “investment value” of a business—its worth to the owner as an ongoing entity rather than its hypothetical sale price. This approach takes into account the considerable time, resources, and effort the owner has invested in the business, acknowledging its intrinsic financial value to them.

How Are Taxes Considered in Business Valuation?

In California family law, courts establish that they cannot reduce the value of assets, including businesses, for potential income taxes unless those taxes are specific, direct, and immediate in relation to the divorce. Courts cannot make assumptions about future taxes. For example, a business’s value cannot be reduced based on anticipated capital gains taxes, even if its tax basis is near zero. Additionally, if one spouse must make an equalization payment to the other to balance the division of assets, that payment is not tax-deductible and must be made with after-tax funds.

What Is the Valuation Date for a Business in a California Divorce?

Typically, the business is valued as close as possible to the trial or settlement date unless the court allows an alternate date. An alternative valuation date may be selected if external circumstances have substantially affected the business’s value or if the business is largely dependent on the work of one spouse. If the business’s revenue is primarily the result of one spouse’s efforts, the court might use the date of separation for valuation purposes, as any increase in value due to post-separation work is typically treated as separate property.

Who Is Generally Awarded Ownership of a Community Business?

In most cases, the court awards the community business to the spouse most actively involved in its operation. Courts seldom order a community business to be sold. If both spouses are crucial to the business, the court will assess which spouse has the best ability to manage the business successfully and contribute to its long-term viability.

How Do You Buy Out Your Spouse’s Share in a Community Business?

It’s uncommon for the court or divorcing spouses to agree to retain joint ownership of a business after the divorce. Since the decision to divorce implies a separation, continued collaboration within the business is generally unrealistic. If one spouse is awarded the business, its value is added to that spouse’s share of the marital asset balance sheet, while other assets (if available) are given to the other spouse. If necessary, the spouse who retains the business may owe an equalization payment to the other. For instance, if the wife is awarded a business valued at $800,000 and the husband is awarded $300,000 in home equity, the wife will need to pay an additional $250,000 to the husband to ensure each spouse has $550,000 in net assets. This equalization payment may include interest if paid over time, typically ranging from one to five years depending on financial factors.

Calculating a Business Owner’s Income for Support Payments

In divorce proceedings, the income derived from a business is often termed “controllable cash flow available for support.” This includes both income or distributions from the business and personal expenses covered by the business, commonly called “perks.” It may also include retained earnings that could reasonably be distributed without compromising the business’s cash flow or working capital. Voluntary contributions to retirement accounts are generally added back to controllable cash flow, as is depreciation in most cases.

Can a Prenuptial Agreement Shield a Business During Divorce?

Yes, a prenuptial agreement created before marriage can adjust the rules governing business ownership in a future divorce. Such agreements can protect the owning spouse’s interests by specifying that income generated from the business and any increase in business value during the marriage are separate property. In essence, a prenuptial agreement can override California’s default laws, allowing the couple to set their own terms, which gives the business owner greater control over the division of business assets in the event of divorce.

Can a Buy-Sell Agreement Signed Post-Marriage Protect the Business?

Generally, a Buy-Sell Agreement signed after marriage does not change each spouse’s rights in a divorce. While it may impact relationships with other shareholders or partners, it typically doesn’t alter the spouses’ rights without independent legal advice at the time of signing and a clear understanding of its impact in a divorce setting.

How Are Accounts Receivable Valued in Business Division?

Accounts receivable are included in a business’s book value. In most cases, accounts receivable are valued after taxes, similar to deferred compensation or stock options, as they only hold value once collected and are then subject to tax.

How Does the Court Determine Whether a Business Is Community or Separate Property?

Whether a business is characterized as community or separate property generally depends on when it was acquired. A business established before marriage is typically considered separate property, though factors such as its management and funding could influence this classification.

Can the Community Acquire a Stake in a Separate Property Business?

The community typically does not acquire ownership in a separate property business unless the owning spouse formally changes the asset’s classification. However, if the business’s value grew considerably during the marriage due to community efforts, the non-owning spouse might have a right to reimbursement for those contributions, though they wouldn’t gain an ownership share in the business itself.

Summary

Divorce cases involving business assets require detailed planning, expert analysis, and strategic preparation. Understanding the court’s approach to dividing assets, recognizing the challenges specific to business valuation, and taking proactive steps to protect your interests are all essential. By seeking mediation, consulting with specialists, and collaborating closely with experienced professionals, you can navigate the complexities of divorce and business ownership in Orange County. Taking these steps can help you manage the process with greater confidence, ensuring that your financial and personal interests are safeguarded during this challenging time.

What Constitutes Separate Property in a Divorce?

In divorce proceedings, separate property refers to assets or items that belong exclusively to one spouse. Typically, separate property includes assets acquired before the marriage, any items obtained individually by a spouse after marriage, and assets received as personal gifts or inheritances during the marriage. The classification of property as “separate” usually hinges on the date of acquisition. If an asset doesn’t meet the criteria for separate property, it is generally considered community property.

In a divorce, the court’s role is to ensure that each spouse retains their separate property. Community property, however, is subject to division. Importantly, courts don’t have to divide every single item in half. Instead, they focus on balancing the overall value awarded to each spouse, aiming for an equal distribution of assets. In certain cases, the court may assign a high-value asset to one spouse and then order them to make an equalization payment to the other spouse to even out the total division.

While equalization payments aim to create fairness, they can sometimes introduce complexities. Spouses may disagree on the amount owed, the interest rate applied, or the duration of the payment schedule. These potential points of contention underscore the importance of properly documenting assets and understanding the difference between separate and community property.

How Are Inheritances and Gifts Allocate in Divorce?

In California, inheritances are generally classified as separate property belonging exclusively to the spouse who received them. This classification applies regardless of when the inheritance was obtained, whether prior to or during the marriage. Consequently, if one spouse inherits money or property, it typically remains their own, and the other spouse has no legal entitlement to it. However, any income generated from the inheritance—such as interest, dividends, or rental income—may still be considered in determining child or spousal support.

Similarly, most gifts given to one spouse during the marriage are typically considered separate property. However, specific legal requirements must be met for an item to qualify as a gift in the legal sense. All types of gifts are not treated in the same way.

Example: Imagine one spouse gifts a car to the other for an anniversary, complete with a celebratory gesture. Despite the intent, this act alone does not satisfy the legal criteria for a valid gift. For the car to be classified as separate property, a written statement transferring ownership is required. This measure is in place to safeguard each spouse’s rights and prevent misunderstandings over ownership if a divorce occurs.

What Qualifies as Community Property in California?

California follows a community property model, which means that assets are divided into separate and community property categories. Community property typically includes any income or property acquired by either spouse during the marriage, from the date of marriage up until separation. This encompasses wages earned by either spouse as well as any property purchased with those earnings. As a result, these assets are generally subject to division in the event of divorce.

However, this community property classification is based on a rebuttable presumption. In some cases, it may be possible to challenge the community property status of an asset. For instance, if a spouse uses an inheritance or a personal gift to purchase a property during the marriage, that property may be classified as separate, provided there is sufficient documentation. In addition, if the title of an asset lists only one spouse, this can serve as evidence that the asset is separate, though title alone does not always definitively establish ownership.

Example: Let’s say a spouse inherits funds during the marriage and subsequently uses them to purchase a property. Because the funds for the purchase originated from an inheritance, the property may remain classified as separate, even though it was bought during the marriage. Clear documentation in these cases is crucial to uphold the asset’s separate status.

How Are Earnings from Separate Property Characterized?

In general, any earnings derived from separate property are also classified as separate, assuming they are not mixed with community funds. For instance, if one spouse owns stocks as separate property, any dividends generated from those stocks are also considered separate property, provided they remain in a distinct account. The same principle applies to other types of income, such as interest earned from a separate savings account or rental income from a solely owned property.

To avoid complications, it is crucial to keep separate property income distinct from community property, as commingling funds can obscure the classification. For example, if dividends from separate property stocks are deposited into a joint account and used for household expenses, those dividends may lose their separate property status.

Examples:

- Dividends from separate stocks are separate property if deposited into a solely held account.

- Interest earned from a separate savings account is classified as separate, provided it’s not mixed with community funds.

- Rental income from a solely owned property retains its separate classification if kept distinct from community finances.

If these earnings are used to acquire a new asset, the new asset generally retains its separate property classification, assuming the original source of funds is documented.

How Is a Separate Property Business Treated in Divorce Cases?

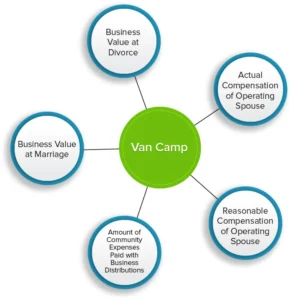

A business owned by one spouse before the marriage is typically considered separate property. However, if the business appreciates in value during the marriage, the community may be entitled to reimbursement if marital efforts or contributions supported the business’s growth. This right to reimbursement can come into play if the owner-spouse actively works in the business during the marriage, resulting in a value increase that indirectly benefits both parties.

Courts usually apply one of two methods to determine community reimbursement: the Van Camp or Periera approach. The Van Camp method is generally used when the business’s growth results mainly from external factors, like investments or favorable market conditions, rather than the direct efforts of the owner-spouse. This approach is particularly relevant for businesses that are capital-intensive. On the other hand, the Periera method applies when the growth can largely be attributed to the owner-spouse’s personal involvement and skill, which is often the case in service-based businesses.

In rare circumstances, if a business undergoes significant changes during the marriage, the court may apply both methods to different periods of the marriage, depending on the factors driving growth at various stages.

Can the Community Gain Ownership in a Separate Property Business?

No, the community and the non-owner spouse cannot acquire an ownership interest in a business that is classified as separate property. However, the community may still have a right to financial reimbursement if the business grows in value due to contributions made during the marriage. For example, if the owner-spouse works in the business without taking an adequate salary, which helps increase its value, the community may be entitled to a share of that growth as compensation for the under-compensated efforts.

Example: If the owner-spouse spends considerable time working in the business without drawing a fair salary, resulting in increased business value, the community may have a right to financial reimbursement for part of that increase.

How Is a Business Valued in a Divorce?

For businesses established or acquired during the marriage, the court typically awards ownership to the spouse actively involved in managing it. To determine the business’s value, courts employ accepted valuation methods, primarily the capitalization of earnings and capitalization of excess earnings approaches. The capitalization of earnings method evaluates the business based on its income-generating ability, while the capitalization of excess earnings approach assesses the business based on its assets.

Significantly, in divorce cases, courts do not speculate on future earnings or potential growth. This differs from other valuation scenarios, where anticipated revenue or growth potential may be included. In a divorce context, historical earnings are capitalized.

Can a Separate Property Business Become Community Property?

A business that starts as separate property can only become community property if the owning spouse signs a formal transmutation agreement. This agreement must clearly state the owner’s intent to convert the business into community property. Informal promises, verbal statements, or casual agreements are insufficient to change the classification legally from separate to community property.

How Can the Community Gain an Interest in a Separate Property Home?

If one spouse owns a home before marriage, that home is considered separate property. However, if community funds are used to pay down the mortgage on that residence during the marriage, the community may gain an interest in the property. This interest reflects the amount paid toward the mortgage principal with community funds and any increase in the property’s value over time resulting from these payments.

Example: If money from a joint account is used to pay the mortgage on a home owned solely by one spouse, the community could be entitled to a portion of the equity attributable to these payments and the appreciation of the real estate.

Determining the Date of Separation

The date of separation refers to the point at which one spouse explicitly and clearly conveys, either through words or actions, that the marriage has ended. This date is critical as it affects the classification of assets, earnings, and debts moving forward. For example, income earned after this date is generally treated as separate property for each spouse. Accurately documenting this date can prevent future disputes over when the marriage officially concluded.

In-Depth Understanding of Spousal Support Law

Our legal team’s comprehensive understanding of spousal support laws enables us to guide Tustin clients through even the most complex situations. Securing the correct ruling at trial is critical, as appellate courts rarely overturn spousal support decisions. We work diligently to ensure that our clients achieve fair and just outcomes at the trial level.

Factors Impacting Spousal Support Orders

Spousal support orders may involve multiple components, including support amount, duration, step-down provisions, and considerations of the marital standard of living. Determining the marital standard is complex, with various formulas and broad judicial discretion. Our expertise helps clients navigate these complexities with clarity and confidence.

Does The Marriage Length Impact Spousal Support Orders?

The length of a marriage is a significant factor in determining spousal support, although differences between marriages of varying durations (e.g., 9 to 15 years) may be more nuanced than expected. The duration of support depends on many factors, all of which our team meticulously evaluates to secure the best outcome.

Do Spousal Support Orders Have Standard Terms?

Some spousal support orders, such as step-down, Ostler-Smith, or Richmond orders, require specialized knowledge to interpret and apply. We ensure our clients understand these orders, including the conditions under which courts may retain jurisdiction or modify support based on life changes.

Can You Modify Spousal Support?

Spousal support is generally modifiable unless specified otherwise. Courts may alter support following major life changes, such as fluctuations in income or health. Our firm has extensive experience guiding clients through the modification process to ensure that support adjustments are fair and reflective of new circumstances.

Is An Inheritance Considered In A Spousal Support Order?

In California, inheritance is considered separate property. However, income derived from an inheritance may be factored into spousal or child support calculations. Our divorce lawyers provide guidance on this issue, helping our Tustin clients understand how inheritance impacts their support obligations.

Conclusion

Choosing the right Tustin family law firm is essential to your case and future. MINYARD MORRIS combines extensive legal experience, strategic focus, and supportive representation to guide Tustin residents through family law challenges. With over 600 divorce lawyers practicing in Orange County, selecting the right attorney may seem overwhelming, but we invite you to explore how our firm can provide the specialized guidance and trusted advice you deserve. Contact us at (949) 724-1111 or reach out through our Initial Consultation page to learn how we can support you in securing the best possible outcome for your case.