Why Minyard Morris Should Handle Your Irvine Divorce

Before hiring an Irvine divorce lawyer, take the time to compare options. A law firm’s website can reveal not only their expertise but also their approach to handling cases like yours. Does their message and mentality align with your values? Do they seem capable of handling the complexities of your case, especially if business ownership is involved? Is that an area they have significant experience?

Divorce is challenging on its own, but when business interests are at stake, the process becomes even more complex. The financial, emotional, and logistical decisions you make during this time can affect your future for years to come. That’s why selecting a knowledgeable divorce lawyer, who services the Irvine area and has extensive experience in business-related cases is crucial.

At Minyard Morris, we understand the stakes. As one of California’s most respected family law firms, we specialize in navigating cases involving small businesses. With 20 divorce lawyers and over 350 years of combined experience, our Orange County team delivers the expertise and personalized service that complex cases require.

In 2024, the esteemed and independent lawyer rating service, Best Lawyers in America® listed 19 of 20 Minyard Morris family law attorneys.

Why Do Irvine Small Business Owners Choose Minyard Morris?

Unmatched Experience

Since 1977, Minyard Morris has built a reputation for excellence, handling some of the most challenging divorce cases in Orange County. We focus exclusively on family law, we do not handle any other matters filed outside of Orange County, bringing deep knowledge of the legal landscape and an unparalleled understanding of local courts, judges, and procedures.

Personalized Strategic Solutions

No two divorces are the same, especially when businesses are involved. Small businesses often present unique challenges, from valuing tangible and intangible assets to determining the value of the business, the terms of any buyout, or even who will be awarded the business. We take the time to understand your unique situation and create a customized plan designed to protect the financial and emotional well-being of our Irvine clients.

Efficient, Client-Focused Representation for Our Irvine Clients

We prioritize efficiency to help you transition from “current client” to “former client” as quickly and as smoothly as possible, our goal from day one is to make our Irvine, California clients “former clients”. By keeping the process focused and transparent, we minimize unnecessary delays and fees, empowering you to move forward with confidence.

The Complexities Of Divorce For Irvine Business Owners

Divorces involving small businesses introduce additional layers of complexity, that generally don’t exist in most other divorces, such as:

- Valuing a Business : Determining a business’s worth is rarely straightforward. Courts may consider tangible assets, goodwill, cash flow, and other factors, often relying on forensic accountants to provide expert valuations.

- Equal Division : California law requires an equal division of community property, which includes the business’s value. If one spouse retains the business, they must compensate the other with assets or payments to achieve an equal division.

- Navigating Financial Strain : Small business owners often face significant financial pressures during a divorce, particularly if their business generates just enough income to cover personal expenses. Additional obligations, like spousal support and attorney fees, can further strain resources.

Strategic Planning: A Cornerstone Of Minyard Morris

At Minyard Morris, our commitment to strategy sets us apart. We hold thrice-weekly meetings, bringing together the collective expertise of 20 divorce lawyers. These sessions ensure that the cases of our Irvine clients benefit from the combined insight of a team with over 350 years of experience.

During these strategy meetings, we:

- Analyze legal nuances, such as recent case law or statutes.

- Develop tailored strategies to address unique challenges, including tactics of opposing counsel or judicial preferences.

Understanding Divorce When A Business Is Involved

Divorce is rarely simple, and when a small business is part of the equation, things can get even more complicated. For business owners in Irvine and Orange County, it is important to understand how courts approach valuing and dividing business interests. Unlike dividing a bank account or personal property, handling a business in a divorce brings unique challenges to our Irvine clients. This article breaks down some of those challenges and offers strategies for navigating them, whether you’re working with a divorce attorney or exploring other options.

If you know how business valuation works, you can play a more active role in your case. That understanding can help you collaborate effectively with your divorce attorney and forensic accountant, making the process smoother and less costly. It can also help you decide whether hiring professionals is the right choice for your situation and whether the resources exist for those experts.

While the fees for a divorce attorney and forensic accountant might seem high, the risks of skipping an expert could cost much more. Imagine spending $25,000 on a divorce attorney, and have the court decrease the value of your business by $150,000 because of the lawyers skilled efforts. That’s a sixfold return on your investment. While no divorce attorney can promise such results, having the right team can make a significant difference in the outcome of your case.

How Are Assets Divided During Divorce?

To understand how a business is handled during a divorce, it helps to know the basics of equally dividing property in California. All community property is split equally between spouses. That doesn’t mean that each item is physically split in half, but rather that both spouses get an equal share of the total value of the marital estate. Accurately valuing assets, including any business interests, is key to creating an equal division of the assets.

For instance, if your business is worth $400,000 and the rest of the community property totals $100,000, the marital estate is valued at $500,000. Each spouse is entitled to $250,000. If one spouse keeps the business, they would owe the other $150,000 to equalize the division. Courts often allow these payments to be spread out over time and will include interest.

Sometimes couples agree to a “global settlement”, where they divide assets without assigning exact values. While uncommon, this can work when, at least, one spouse is willing to take less than their fifty percent share of the community estate. These decisions must come from the spouse themselves, not their divorce lawyer. Accepting less than fifty percent of the community estate requires a waiver of community property rights.

What Are The Difficulties In Valuing A Small Business In A Divorce?

Valuing a small business in a divorce isn’t always straightforward. Unlike larger companies, small businesses often depend heavily on the owner’s reputation, client relationships, and specialized skills. An experienced divorce attorney and forensic accountant can help assess the business’s value accurately. They’ll look at factors like goodwill, cash flow, accounts receivable, equipment, liabilities, and many others.

Of course, hiring these experts can be expensive and problematic, especially if the business barely earns enough income to pay personal living expenses. Many small businesses are essentially jobs for their owners rather than a viable company. This makes separating personal and business finances challenging. Add in the costs of support obligations and legal fees, an it is not surprising that some Irvine clients feel overwhelmed.

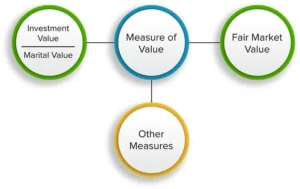

Courts usually determine the “investment value” of a business. Essentially, what is the value of the business to the owner who operates it? This avoids the use of the valuation market approach, which is problematic, and speculation about what the business might sell for and its future income if it wasn’t sold.

How Do The Orange County Courts Value Businesses?

In Orange County, family law courts use two main methods to value businesses: capitalization of excess earnings (an asset-based approach) and capitalization of earnings (an income-based approach). These methods rely on actual financial data and avoid speculative valuation techniques like discounted cash flow (DCF) analysis, which projects future earnings which isn’t allowed in family law cases.

Courts also avoid using “rules of thumb” that apply multiples to value businesses. While these shortcuts are common in other contexts, they don’t hold up in family law because they lack a solid foundation as to the formulas and how they were created. For example, a rule like “two times gross sales” doesn’t consider details like location, transaction terms, market conditions, new competitors, increase rent, loss of key employee, etc.

What Is An In-Place Value?

If a business doesn’t have goodwill or significant profitability, the court might assign it an “in-place” value. This reflects the intangible assets of the business, like its location, website, and existing customer base. While typically lower than goodwill, this valuation acknowledges the effort and resources that went into establishing the business.

Are There Misunderstandings About Business Valuation?

It’s a common misconception that a business has no value if it’s entirely dependent on the owner’s efforts. Orange County courts, however, must assign value to all community assets, even if the business’s worth is modest. Similarly, while courts can’t force someone to continue running a business, closing it improperly could lead to claims of waste or a breach of fiduciary duties.

What Are Some Important Considerations For Business Owners Considering A Divorce?

- Pre-Marital Ownership : If you owned the business before getting married, it’s considered separate property. However, if its value grew during the marriage, the community might have a claim for financial reimbursement for its contributions of time or money.

- Support Payments : It might seem unfair to buyout your spouse’s share of the business and still pay support from the profits. Which were generated through a buyout and was not reduced in value as a result of this “restriction” on the profitability of the business that they purchased for 100% of its value without any discount. California law treats these as separate unrelated issues.

- Retirement or Closure : If you’re 65 or older, the court can’t force you to keep running the business. That said, closing or selling it requires careful planning to avoid claims of waste or breach of fiduciary duties.

- Fiduciary Duties : Starting a ‘competing’ business while still married could violate fiduciary obligations and lead to serious legal consequences.

How Do Courts Address Alternate Valuation Dates And Income Tax Issues, In A Divorce?

Business valuations are usually based on the date closest to trial or settlement. For businesses that rely on personal services, the valuation date might align with the date of separation to account for the operator’s contributions after the marriage has ended. Courts must avoid considering speculative future events, like potential growth or competition, when valuing businesses.

Future taxes aren’t considered by divorce courts unless they’re immediate, specific, and directly related to the divorce itself. An exception to this tax rule are the accounts receivable which are usually valued after accounting for taxes.

What Are Your Options For Legal Representation In An Orange County Divorce?

While it is possible to represent yourself, doing so comes with risks, especially if your spouse hires experienced professionals. Without strong evidence or expert testimony, the court may undervalue or overvalue your business. If you are worried about the cost of full representation, there are alternatives:

- Mediation : Mediation can be an affordable way to resolve disagreements over business valuation and property division. Orange County mediators often recommend hiring a joint forensic accountant to provide a neutral valuation report that both spouses can work with.

- Limited Scope Representation : Also called unbundled services, this option lets you hire a divorce attorney for specific parts of your case, such as handling business valuation, while you manage the rest on your own.

- Consulting Services : You could also work with a less experienced divorce attorney or forensic accountant in a consulting role. This provides guidance at a lower cost and helps you prepare for negotiations or court proceedings.

Should Self-Represented Irvine Residents Carefully Prepare For A Divorce?

If you decide to represent yourself, preparation is key. Consider consulting with affordable divorce attorneys or forensic accountants to learn the basics. Look for online resources about business valuations in California divorces and visit the Supreme Courts Facilitator’s office (self help) in Orange, for help with paperwork. Watching hearings in your judge’s courtroom can also provide valuable insight along with watching You Tube videos or trial practice.

When You Are Ready, Consult With An Irvine Divorce Lawyer

Selecting the right Irvine attorney for your divorce is critical. With over 600 divorce lawyers in Orange County, the process of choosing can feel overwhelming. At Minyard Morris, we stand out for our unwavering commitment to strategy, collaboration, and client success. For over 48 years, our firm has been a trusted name in family law, consistently delivering outstanding results.

If you have a small business and are getting a divorce, take the next step and call us at (949)724-1111. Or reach out via our online consultation form. Let us provide the guidance and representation you need to navigate your divorce with confidence.