Why Choose Minyard Morris for Your Orange County Divorce?

Selecting the right divorce lawyer is one of the most critical decisions you’ll face. When small business ownership is involved, the stakes are even higher. The outcome of the case will significantly influence your financial future, and your long-term goals. At Minyard Morris, we understand the unique challenges business owners encounter during a divorce and are here to expedite the proof towards a favorable result.

With over 48 years of experience and more than 350 years of combined attorney expertise, our firm is a trusted name in Orange County family law. Our 20 divorce lawyers work collaboratively to provide personalized strategies that align with our Costa Mesa clients’ goals.

In 2024, the esteemed and independent lawyer rating service, Best Lawyers in America® listed 19 of 20 Minyard Morris family law attorneys.

Challenges For Business Owners When Divorcing

Divorce is always a difficult process, but owning a business adds even more complexity. Key issues include:

- Business Valuation: Small businesses can be difficult to value accurately due to factors like goodwill, accounts receivable, dependent on the owner’s reputation and skills, and less than perfect records.

- Asset Division: California’s community property laws mandate equal division pf marital assets. Determining the value of a business and how it fits into this division is rarely straightforward.

- Financial Pressure: Divorce can strain cash flow, particularly for business owners balancing operational needs, personal expenses, support, and legal costs.

These complexities demand a nuanced approach, and at Minyard Morris, we pride ourselves on crafting strategies tailored to protect your business, assets, and future.

How Minyard Morris Excels In Complex Cases

Our firm’s approach to strategy is on thing that sets us apart. Three times a week— Mondays at 5:00 p.m., Tuesdays at noon, and Thursdays at noon— our entire team of 20 divorce attorneys gathers for in-depth discussions about our Costa Mesa cases. The collaborative environment ensures every case benefits from our collective expertise. We start by:

- Crafting detailed strategies for unique legal challenges.

- Staying up-to-date on the latest family law trends, local judicial preferences, and latest seminars.

- Analyze settlement options and trial tactics to align with our Costa Mesa clients’ goals.

For our Costa Mesa clients, this approach provides a distinct and unique advantage— having access to a team of 20 divorce attorneys that brings over three centuries of combined legal knowledge that they leverage for our clients.

Divorce And Business: Navigating The Maze Of Case Law

Divorce is rarely a straightforward process, and when a small business is part of the marital estate, the challenges multiply. A divorce with a business is an entirely different case and requires a divorce lawyer with a specific skill set, education, and experience that is not necessary for the traditional divorce. For business owners in Orange County, understanding how the courts approach the valuation and division of the business is critical. Unlike other types of assets, such as personal property or financial accounts, businesses introduce layers of complexity that require careful handling. This article outlines some of the key issues and offers insights to help you navigate this aspect of your divorce, whether you work with an experienced divorce attorney or explore other representation options.

Knowing the basics of business valuation can significantly improve your ability to work with your divorce attorney and forensic accountant. With a better understanding of the process, you can reduce fees, improve efficiency, and make informed decisions about your legal strategy. For small business owners, this knowledge is especially valuable because of the importance involved.

Hiring a divorce attorney and forensic accountant can be costly, but the potential financial risks of engaging professionals could be significantly higher. For example, investing $50,000 in legal representation might result in a court-assigned business valuation of $300,000, lower than initially claimed by your spouse. That’s a sixfold return on your investment. While no divorce attorney can guarantee such results, the impact of skilled representation on your financial future can be significant.

How Are Assets Divided In Divorce?

To understand how businesses are handled during a divorce, it’s important to first grasp the rules governing property division. Community property must be equally divided. Accurate valuation of all community assets, including any business interests, is essential to this process.

For instance, suppose your business is valued at $600,000 and the couple’s remaining community property totals $500,000 The marital estate is worth $1,100,000, and each spouse is entitled to $550,000. To equalize the division, the spouse retaining the business would owe $150,000 to the other, assuming the other party retained all of the other assets. Because such payments can strain liquidity, courts often allow structured payments over time, sometimes including interest or security provisions

On occasion, couples may agree for a “global settlement”, agreeing to divide assets without attempting to arrive at values. This approach can work when one party willingly accepts less than their fair share of the estate. Global agreement can be the result of a mediation or a settlement negotiated by the lawyers.

What Are The Difficulties Relative To A Small Business And Divorce?

Valuing a small business during divorce is rarely simple. Unlike larger companies, small businesses often rely on the owner’s reputation, and client relationships. Engaging a skilled divorce attorney and a forensic accountant is essential. These professionals assess a variety of factors, including goodwill, cash flow, accounts receivable, physical assets, and liabilities to arrive at a value.

However, the costs of hiring these experts can be significant and problematic. Many small businesses are essentially jobs for their owners. Adding support obligations and legal fees to the mix makes funding the process even more challenging.

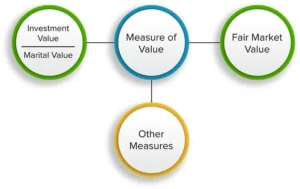

Courts usually determine the “investment value” of a business, which is the value to the owner who runs it— rather than focusing on its market value or potential sale price

How Does The Orange County Court Value Small Businesses?

Family law courts in Orange County use two primary methods for valuing businesses: The capitalization of excess earnings method (an asset-based approach) and the capitalization of earnings method (an income-based approach). Both methods rely on historical income not projected future income.

Courts also avoid using industry-specific “rules of thumb”, which apply specific formulas to business valuations. While these rules are used in other fields, they don’t hold up in family law because they lack solid evidentiary support. Rules of thumb may be appropriate to get a ‘baseball’ value. For example, a formula like “two times gross sales” fails to account for critical factors like geographic location, market conditions, or transaction terms.

What Is An ‘In-Place’ Value?

When a business doesn’t generate goodwill or significant profits, courts may assign it an “in-place” value. This reflects the operational aspects of the business— such as its location, website, and customer base— that make it a functioning enterprise. While typically lower than goodwill, this value recognizes the work that went into establishing the business as it exists at that point.

What Other Considerations Are Relevant To Small Business Owners?

- Pre-Marital Ownership: If you owned the business before getting married, it is your separate property. However, if its value increased during the marriage, the community may have a claim of financial reimbursement.

- Retirement or Closure: Courts cannot require business owners aged 65 or older to continue operating a business. However, plans to sell or close the business must be done with notice and court consent to avoid claims of waste or breach of fiduciary duty.

- Fiduciary Obligations: Starting a business, competing with the community, while still married would breach fiduciary duties, potentially leading to serious legal consequences and sanctions.

What Unique Aspects Exists Relative To An Alternate Valuation?

Business valuations are typically based on the date closest and most practical to trial or settlement. For businesses dependent on personal services, the valuation date may be the separation date to reflect the operator’s post-separation efforts.

Income taxes are generally excluded from valuations unless they are immediate, specific, and directly related to the divorce. One application of the rule, accounts receivable are often valued after taxes are considered, but this is typically resolved by the time of trial or settlement.

Are Legal Representation Options Serious Considerations?

While self-representation is an option, it comes with considerable risks, particularly if your spouse hires an experienced legal team. Without strong evidence or expert testimony, the court may arrive at an unfavorable or incorrect valuation for your business. If the cost of full legal representation is prohibitive, you might consider these alternatives:

- Mediation: Mediation can be a cost-effective way to resolve disputes over business valuation and property division. A mediator might suggest hiring a neutral forensic accountant to provide valuation and other reports.

- Limited Scope Representation: Also known as unbundled legal services, this option allows you to hire a divorce attorney for specific parts of your case—like business valuation— while managing other aspects on your own.

- Consulting Professionals: Hiring a less experienced divorce attorney or forensic accountant in a consulting role can provide valuable guidance at a lower cost, helping you prepare negotiations or court proceedings.

Is Preparing For Self-Representation An Important Plan

If you choose to represent yourself, preparation is critical. Consulting with affordable divorce attorneys or forensic accountants can provide valuable insights. Additionally, online resources, Superior Courthouse court facilitator services (self-help center), and observing hearings in your assigned judge’s courtroom can help you understand the process and improve your presentation.

Experiencing A Divorce In Costa Mesa? Consult With A Divorce Attorney When You Are Ready

Selecting the right Costa Mesa attorney for your divorce is critical. With over 600 divorce lawyers in Orange County, the process of choosing can feel overwhelming. At Minyard Morris, we stand out for our unwavering commitment to strategy, collaboration, and client success. For over 48 years, our firm has been a trusted name in family law, consistently delivering outstanding results.

If you have a small business and are getting a divorce, take the next step and call us at (949)724-1111. Or reach out via our online consultation form. Let us provide the guidance and representation you need to navigate your divorce with confidence.