Divorce is hard enough on its own, but when valuable assets or business interests are involved, it can get especially complicated. The decisions you make during this time can shape your financial security, emotional well-being, and future stability for years to come. That’s why having an experienced divorce lawyer who understands not just family law but also the complexities of dividing business assets is so important. With the right legal support, you can move through this process more smoothly and make sure you’re getting a favorable outcome.

At Minyard Morris, we know how important it is to feel secure and supported by your legal team during such a major life change. We’re honored to be one of the nation’s top family law firms, trusted for handling even the toughest, most high-stakes divorce cases with care, expertise, and a true sense of urgency. Our team is made up of 20 skilled divorce lawyers who focus exclusively on family law cases filed in Orange County. With more than 350 years of combined experience, we bring a high level of knowledge and insight to every case, and we’re ready to dive into even the most complex issues with a personalized, strategic approach.

We know that every divorce case is different, especially when it comes to dividing businesses, complex financial holdings, or high-value assets. These situations require more than just a standard approach; they need an understanding of your unique circumstances, and a strategy built around your specific goals. At Minyard Morris, we take the time to understand the details of our Irvine client’s cases so we can develop a game plan tailored to your needs. We don’t believe in “one-size-fits-all” solutions. Instead, we dig into the details, making sure we’re fully informed and prepared to advocate for you effectively.

We also know that going through a divorce, especially one with a lot of financial complexity, can be incredibly stressful. Our goal is to make the process feel as manageable as possible, keeping our Irvine clients informed and supported from start to finish. You’re not just a case to us; we prioritize you as a person, making sure your questions get answered and your concerns are heard. Whether it’s offering guidance, addressing your worries, or helping you make the tough decisions, we’re here to stand by you and make sure your choices align with what matters most to you.

One of our top priorities is to help our Irvine clients transition smoothly from “current client” to “former client” without dragging out the process. We know that nobody wants a divorce to go on any longer than necessary, and we share that commitment. Our team works efficiently and keeps a close eye on every detail, moving things forward as quickly as possible while making sure no corners are cut. We’re focused on getting our Irvine client the best possible result, without unnecessary delays, so you can move forward with confidence and peace of mind.

We also believe that a strong attorney-client relationship relies on trust and transparency. You deserve to know what’s happening with your case at every stage, so we prioritize open, clear communication. Our divorce lawyers take the time to explain things in straightforward terms, ensuring you understand each step of the process and can make decisions with confidence. We don’t just want to handle your case—we want to empower you by making sure you’re part of the process and fully informed.

Choosing the right family law firm is a big decision, especially when it involves protecting your future and financial well-being. At Minyard Morris, you’re choosing a team of professionals who are not only highly skilled but also genuinely care about helping you achieve the best possible outcome. We understand that divorce can feel overwhelming, but we’re here to offer steady guidance and practical advice every step of the way. From your initial consultation to the final judgement, we’re focused on standing up for your best interests and helping you move forward with clarity and peace of mind.

If you’re going through a divorce that involves substantial assets or business interests, Minyard Morris is here to help. Our experienced, dedicated team of 20 divorce lawyers is prepared to make your case a top priority, delivering both strong representation and compassionate support. Every Irvine client deserves a divorce lawyer who respects and values them, and at Minyard Morris, we strive to provide exactly that. We’re here to help you navigate this major life transition with confidence, understanding, and the peace of mind you deserve.

The Power Of Collaboration: Inside Our Firm’s Unique Strategy Sessions

For decades, Minyard Morris has embraced a collaborative approach that sets us apart. Our team of skilled family law attorneys comes together three times a week—Monday at 5:00 p.m., Tuesday at noon, and Thursday at noon—for in-depth strategy sessions. This commitment isn’t just a tradition; it’s a cornerstone of how we achieve the best results for our clients.

With over 350 years of combined legal experience in the room, these meetings are an essential part of our practice. Picture this: all 20 of our attorneys gather around the table, ready to dissect the intricacies of ongoing cases. Attendance isn’t just encouraged; it’s expected. Why? Because every lawyer’s insight is a valuable piece of the puzzle, and we believe that the best solutions come from collective thinking.

What Happens Behind Closed Doors?

During these sessions, no topic is off-limits. We discuss how to handle specific opposing counsel, unique ways to approach the assigned judicial officer, relevant case law, new appellate court rulings, recent seminars, and even similar cases we’ve tackled before. Discussions cover every angle—from evidentiary issues and trial strategies to settlement options and the potential value of what’s at stake. The exchange of ideas is endless, and that’s exactly what gives us an edge.

It’s no secret within the family law community that we conduct these weekly gatherings. Other attorneys and even judicial officers often express curiosity about our unique approach. In fact, our collaborative model attracts talented lawyers who want to be part of something bigger. After all, how many firms can say they leverage the collective experience of 20 family law experts in every single case?

Why This Matters To Our Clients

The benefits of these meetings are profound, even if not easily quantified. Clients often wonder: “Would I rather have a lawyer backed by a team of 19 other family law specialists exclusively practicing in Orange County, or one who consults with just one or two peers at a smaller firm?” The answer is clear.

Consider this: one of our lawyers may question if there’s legal support for a specific position. Instead of spending hours on research, they bring it to the meeting. Often, another attorney recalls a similar case, providing immediate insights and citing relevant appellate court decisions. This level of shared knowledge means more efficient, informed decision-making for our clients.

Sometimes, our attorneys seek a “reality check” from their peers, or we debate the odds of winning a particular issue before a specific judicial officer. Other discussions revolve around which expert witness would best strengthen a case. Perhaps the most valuable outcome of these sessions is the brainstorming around settlements—how to structure them and creatively overcome potential roadblocks. The variety of issues we address is virtually limitless.

An Unmatched Commitment to Excellence

You might wonder about the cost of this level of collaboration. Truthfully, it’s significant. We devote the time of 20 lawyers to these thrice-weekly meetings, and not a minute of it is billed to our clients. With hourly rates ranging from $350 to $800, the internal cost adds up quickly. Yet, we continue this practice because we believe it’s invaluable to the representation we provide.

Sure, other firms might informally chat about cases. But none invest in this level of consistent, in-depth collaboration like Minyard Morris. It’s one of the key elements that sets us apart, and our clients recognize the difference. We’re committed to offering top-notch service and achieving the best outcomes, and our collaborative meetings play a pivotal role in making that happen.

Why Hiring Both A Family Law Attorney And A Forensic Accountant Is Essential

Hiring a family law attorney and a forensic accountant may seem like a large expense, but the costs of not retaining these experts could be far greater. The central question to consider is: what financial repercussions might there be if you don’t hire a lawyer and accountant to ensure an accurate business valuation? An incorrect valuation could lead to significant financial losses. Engaging an experienced family law attorney in Orange County may turn out to be one of the best financial choices you make in a divorce, especially when you factor in the difference between a professional valuation and an uninformed estimate. Familiarizing yourself with these issues can also help you work more closely with your attorney and forensic accountant, which may ultimately reduce expenses.

Is An Expert Required For Valuing A Business In Divorce?

While a business owner can technically offer testimony regarding the value of their business, the court often finds this testimony less persuasive, especially if the other party has hired an experienced valuation expert. Business owners typically lack the specific legal knowledge related to valuation issues in family law cases and the rules of evidence that are necessary to present a compelling case. This gap in knowledge could limit their ability to testify effectively or even prevent certain documents from being admitted into evidence.

In contrast, a qualified valuation expert provides a substantiated opinion based on thorough research and analysis. Courts generally place greater trust in the assessment of a qualified expert than in the subjective valuation of a business owner. While a family law attorney can collaborate with a forensic expert to build a comprehensive case, the attorney alone cannot offer a professional business valuation. Without a forensic accountant, a divorce case involving a business lacks the complete team necessary to present a compelling, evidence-backed business valuation. Ultimately, the court will assess which side has presented the more reliable evidence, and it’s highly unlikely that a judge would rely solely on the business owner’s personal opinion.

What Information Must Be Disclosed To Your Spouse About The Business?

As a business owner, you are required by law to provide your spouse with all relevant information regarding the business. Determining what constitutes “relevant” information can be challenging, but a wise approach is to consider, “What would I want to know if I were on the other side of this case?” Over-disclosure is generally recommended to minimize the risk of having your settlement or judgment revisited later. Over-disclosure means providing any documents and information that could impact the valuation of the business. Some advisors suggest that a business owner should disclose any information they would want to know if they were considering purchasing the business. Sharing full details with your family law attorney can also help them guide you more effectively throughout the process.

Should You Wait To Be Asked For Documentation Or Disclose Voluntarily?

No, waiting for your spouse to request documents is insufficient. California law requires business owners to voluntarily provide all significant information to the other party. This includes both physical documents and verbal information, such as any informal offers to buy the business.

What Are The Consequences Of Failing To Disclose Key Business Details?

Failure to disclose material business information can result in serious penalties. Depending on the circumstances, including any intent, motivation, or malice behind the omission, penalties can include awarding the other party 50% to 100% of damages incurred due to the lack of disclosure, as well as significant attorney fees. Full, proactive disclosure is the best way to avoid these risks and to ensure that you are meeting your legal obligations.

Must You Disclose Any Offer Received To Purchase The Business?

Yes, any offer to purchase the business, even if it was only verbal or did not result in a sale, is considered a material fact that must be disclosed. Details regarding the terms, proposed price, and the potential buyer’s identity could be critical in assessing the business’s value in divorce proceedings.

Is Disclosure Required For A Recent Business Appraisal?

Yes, any recent business appraisal must be disclosed, regardless of the reason it was conducted, the date it was completed, or the valuation methods used. Courts consider past appraisals highly relevant in assessing the business’s current value, even if the appraisals were initially performed outside the divorce context.

Final Declarations Of Disclosure: What Are They, And Are They Mandatory?

California’s Family Code requires both spouses to exchange Preliminary Declarations of Disclosure, followed by Final Declarations of Disclosure. Preliminary disclosures are mandatory and cannot be waived, while Final Declarations may be waived if both parties consent. However, even if the formal Final Declaration is waived, the obligation to provide fully updated and accurate information remains. In other words, while the document itself can be waived, full transparency regarding the business’s financial status and value is still required.

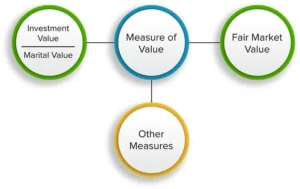

What Is The Investment Value Of A Business In Divorce Proceedings?

In divorce cases, businesses are not always assessed based on fair market value. Many businesses may not be sellable at a price that reflects their true worth to the owner, yet they can still have significant “investment value.” A common misconception is that a business lacks value if it relies heavily on the spouse who operates it. While some businesses depend on the owner’s involvement, courts in Orange County often calculate the “investment value” of a business—its worth to the owner as an ongoing entity rather than its hypothetical sale price. This approach takes into account the considerable time, resources, and effort the owner has invested in the business, acknowledging its intrinsic value to them.

How Are Taxes Considered In Business Valuation?

In California family law, courts establish that they cannot reduce the value of assets, including businesses, for potential income taxes unless those taxes are specific, direct, and immediate in relation to the divorce. Courts cannot make assumptions about future taxes. For example, a business’s value cannot be reduced based on anticipated capital gains taxes, even if its tax basis is near zero. Additionally, if one spouse must make an equalization payment to the other to balance the division of assets, that payment is not tax-deductible and must be made with after-tax funds.

What Is The Valuation Date For A Business In Divorce?

Typically, the business is valued as close as possible to the trial or settlement date unless the court allows an alternate date. An alternative valuation date may be selected if external circumstances have substantially affected the business’s value or if the business is largely dependent on the work of one spouse. If the business’s revenue is primarily the result of one spouse’s efforts, the court might use the date of separation for valuation purposes, as any increase in value due to post-separation work is typically treated as separate property.

Who Is Generally Awarded Ownership Of A Community Business?

In most cases, the court awards the community business to the spouse actively involved in its operation. Courts seldom order a community business to be sold. If both spouses are crucial to the business, the court will assess which spouse has the best ability to manage the business successfully and contribute to its long-term viability.

How Can You Buy Out Your Spouse’s Share In A Community Business?

It’s uncommon for the court or divorcing spouses to agree to retain joint ownership of a business after the divorce. Since the decision to divorce implies a separation, continued collaboration within the business is generally unrealistic. If one spouse is awarded the business, its value is added to that spouse’s share of the marital asset balance sheet, while other assets (if available) are given to the other spouse. If necessary, the spouse who retains the business may owe an equalization payment to the other. For instance, if the wife is awarded a business valued at $400,000 and the husband is awarded $200,000 in home equity, the wife may need to pay an additional $100,000 to the husband to ensure each spouse has $300,000 in net assets. This equalization payment may include interest if paid over time, typically ranging from one to four years depending on financial factors.

How Does Business Ownership Impact Spousal Support?

The spouse awarded the business is expected to generate income from it, which will be considered in spousal support calculations. In a divorce, the business’s value to the awarded spouse may be somewhat diminished, as part of its income may be allocated toward spousal support. This setup, often referred to as “double-dipping,” has been upheld by appellate courts as fair. If the business were sold and each spouse had separate employment incomes, support would be calculated based on those individual earnings.

Calculating A Business Owner’s Income for Support Payments

In divorce proceedings, the income derived from a business is often termed “controllable cash flow available for support.” This includes both income or distributions from the business and personal expenses covered by the business, commonly called “perks.” It may also include retained earnings that could reasonably be distributed without compromising the business’s cash flow or working capital. Voluntary contributions to retirement accounts are generally added back to controllable cash flow, as is depreciation in most cases.

Can A Prenuptial Agreement Shield A Business During Divorce?

Yes, a prenuptial agreement created before marriage can adjust the rules governing business ownership in a future divorce. Such agreements can protect the owning spouse’s interests by specifying that income generated from the business and any increase in business value during the marriage are separate property. In essence, a prenuptial agreement can override California’s default laws, allowing the couple to set their own terms, which gives the business owner greater control over the division of business assets in the event of divorce.

Can A Buy-Sell Agreement Signed Post-Marriage Protect The Business?

Generally, a Buy-Sell Agreement signed after marriage does not change each spouse’s rights in a divorce. While it may influence relationships with other shareholders or partners, it typically doesn’t alter the spouses’ rights without independent legal advice and a clear understanding of its impact in a divorce setting.

How Are Accounts Receivable Valued In Business Division?

Accounts receivable are typically included in a business’s book value. The process often involves distinguishing between collectible and non-collectible receivables. This issue can become contentious if accounts receivable are written off during the divorce. In most cases, accounts receivable are valued after taxes, similar to deferred compensation or stock options, as they only hold value once collected and are then subject to tax.

Determining Whether A Business Is Community Or Separate Property

Whether a business is classified as community or separate property generally depends on when it was acquired. A business established before marriage is typically considered separate property, though factors such as its management and funding could influence this classification. If a business’s value has significantly increased during the marriage due to contributions from the community, the non-owning spouse may be entitled to reimbursement, though they may not receive a direct ownership interest.

Can The Community Acquire A Stake In A Separate Property Business?

The community typically does not acquire ownership in a separate property business unless the owning spouse formally changes the asset’s classification. However, if the business’s value grew considerably during the marriage due to community efforts, the non-owning spouse might have a right to reimbursement for those contributions, though they wouldn’t gain an ownership share in the business itself.

Summary

Divorce cases involving business assets require detailed planning, expert analysis, and strategic preparation. Understanding the court’s approach to dividing assets, recognizing the challenges specific to business valuation, and taking proactive steps to protect your interests are all essential. By seeking mediation, consulting with specialists, and collaborating closely with experienced professionals, you can navigate the complexities of divorce and business ownership in Orange County. Taking these steps can help you manage the process with greater confidence, ensuring that your financial and personal interests are safeguarded during this challenging time.

A Clear Breakdown Of Separate Property In A California Divorce

Divorce can get complicated, especially when it comes to dividing up assets. In California, knowing the difference between separate property and community property is key to understanding how everything will be split between spouses. The way these two categories are treated plays a big part in the outcome of the divorce. This guide walks you through what separate property means, how it ties into community property, and how both are dealt with during a divorce.

What Exactly Is Separate Property?

In California, separate property refers to anything that belongs solely to one spouse. This typically happens in a few situations:

- Property owned before marriage: Anything a spouse brought into the marriage is usually considered separate.

- Gifts or inheritances: Things that are given to or inherited by one spouse, no matter when they’re received, stay that spouse’s separate property.

- Property acquired after separation: Once a couple is legally separated, anything one spouse acquires is considered separate property.

The timing and how the property was acquired are key to deciding whether it’s separate or community property. Community property, on the other hand, includes everything either spouse earned or bought during the marriage. When a divorce happens, community property is generally split equally between both spouses. But that doesn’t mean each asset is literally cut in half—it just means the overall value of the community assets is shared fairly. Sometimes, one spouse might need to make an equalization payment to ensure a balanced division.

Protecting Gifts And Inheritances As Separate Property

In California, gifts and inheritances remain separate property, even if they’re received during the marriage. However, it’s important to keep those assets separate and not mix them up with community property.

For example, if you inherit money and deposit it into a joint account with your spouse, it can be hard to tell what’s separate and what’s community property. This can lead to the inheritance being considered part of the community and subject to division. To avoid that, it’s best to keep gifts and inheritances in a separate account to make sure they don’t get mixed with marital funds.

Separate Property Businesses: Navigating The Complications

When one spouse owns a business before marriage, it’s usually considered their separate property. But if the business grows during the marriage—especially because of the owner-spouse’s hard work—the community may be entitled to a share of that increased value.

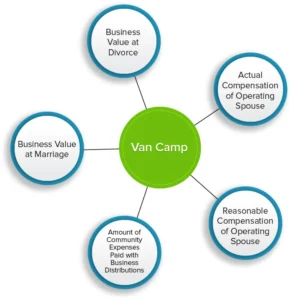

California courts use two main approaches to figure out how much of the business’s growth should go to the community:

- Van Camp Method: This is used when the growth is mostly due to external factors, like investments or the market, rather than the owner-spouse’s efforts. The community usually gets the reasonable value of the owner’s labor during the marriage.

- Pereira Method: This approach is applied when the business’s success is mainly due to the owner-spouse’s personal work and involvement. The community would get a portion of the business’s increase in value, after accounting for a fair return on the owner-spouse’s separate interest.

In rare cases, both methods might be used if the business’s nature changed significantly during the marriage. It’s important to note, though, that the non-owner spouse doesn’t get ownership of the business itself—they’re only entitled to financial compensation for the business’s growth during the marriage.

Valuing A Business In Divorce

If a business was formed or purchased during the marriage, it’s typically considered community property. Generally, the spouse who actively runs the business will keep it, but the court first needs to figure out its value. Valuing a business can be a tricky process, often requiring financial experts like forensic accountants.

Two common methods for valuing businesses are:

- Capitalization of Earnings: This method projects the business’s future earnings based on its current performance.

- Capitalization of Excess Earnings: This method looks at the business’s assets and calculates the return generated from them.

The goal is to determine the investment value of the business to the spouse who will keep it, which can be different from its market value. If the court orders an equalization payment, it’s calculated on an after-tax basis and isn’t tax-deductible for the paying spouse.

Homes Owned Before Marriage: How the Moore Marsden Formula Comes In

If one spouse owns a home before marriage, that home is considered their separate property. However, if community funds—like joint income—are used to pay down the mortgage or improve the home, the community may gain an interest in the property.

To figure out the community’s share of the home’s value, the court uses the Moore Marsden formula. This calculation takes into account how much of the mortgage was paid with community funds and how much the home appreciated in value during the marriage. This ensures that the non-owning spouse gets a fair share of the appreciation that’s due to community contributions.

If the owner wants to change the home’s status to community property, they’ll need to sign a transmutation agreement. This is a written agreement that clearly states the intention to change ownership. Verbal promises or casual conversations won’t cut it under California law.

Why The Date Of Separation Matters

In California, the date of separation plays a major role because it marks the point when community property stops accumulating. Anything acquired after this date is considered separate property.

To establish the separation date, there needs to be clear evidence that one spouse has made it obvious the marriage is over, either by what they said or did. Simply living apart or taking a break doesn’t necessarily mean you’re legally separated unless there’s clear intent to end the relationship for good.

Documenting the separation in writing, like through an email or letter, can help avoid arguments later. The date of separation can have a big impact on how assets are divided, spousal support calculations, and responsibility for post-separation debts.

Handling Money After Separation: Managing Shared Expenses

Once the date of separation is set, each spouse’s earnings are treated as separate property. But complications can arise if one spouse uses their post-separation income to cover community expenses, such as paying off joint debts or the mortgage. In these cases, the spouse who makes the payments might be entitled to reimbursement, unless the expenses were only for their benefit.

To avoid confusion and disagreements, it’s recommended that spouses quickly separate their finances once they’ve decided to split. This means closing joint accounts, stopping the use of shared credit cards, and setting clear financial boundaries moving forward.

Tips For Protecting Your Financial Interests During Separation

To safeguard your financial situation during a separation, here are a few steps you should consider:

- Open a new bank account just for your own income.

- Close any joint accounts and get separate credit cards.

- Change the passwords for all your personal and financial accounts.

- If you’re on a shared phone plan, think about switching to an individual plan.

- Set up a new email account specifically for communicating with your lawyer.

- Stay off social media, or at least minimize your activity, until your divorce is finalized.

- Always consult with a lawyer before making any major financial decisions, like big purchases or investments.

When You Are Ready, Consult With An Experienced Irvine Divorce Lawyer

A consultation is important, as in it, we will assist you in establishing your goals addressing your concerns. Please contact us today at 949-724-1111 or send us an email to schedule your confidential initial consultation with one of our Irvine divorce lawyers.