Divorce is a complex and emotionally taxing process, particularly when a business is involved. For business owners involved in a divorce, understanding how the courts address the valuation and division of a business is crucial. Unlike the straightforward division of simpler assets, a business adds layers of complexity to the divorce proceedings. This article aims to shed light on this intricate process and offer guidance to those dealing with these issues.

This article is intended to assist you in working with your family law attorney. The more you understand about the process of business valuation, the more valuable you will be to your Irvine family law attorney and a forensic accountant in the process and the more efficient and cost effective the process can be.

Affording a family law attorney and a forensic accountant can be problematic for many people. The question to be asked is: What may be the financial cost if you don’t have a lawyer and an accountant, in terms of a incorrect or unrealistic value of your business? The fees you pay a family law attorney in an Orange County divorce may end up being your best investment ever, when considering what the business was versus what it might have been had you not hired experts. Understanding the issues can help you be a better partner with your professionals and minimize costs.

Do You Need An Expert To Value A Business In A Divorce?

Technically, the owner of a business may testify to its value. However, the weight and value of that testimony will likely not be persuasive to a court, especially if the other party has retained an experienced valuation expert. It is likely that the owner of a business will not understand the legal issues involved in the valuation process specific to family law or the rules of evidence, which may prevent him from testifying and prevent his supporting documents from being admitted into evidence. The expert will testify as to the value of the business after having done extensive research and analysis relative to the business. The judicial officer will likely be familiar with the expert, his experience and his credibility.

A family law attorney works with the forensic expert but cannot render an opinion on the value of a business. Having only an attorney does not complete the team needed for a divorce if there is a business involved. The court will determine which side has the more persuasive evidence of value and make its order accordingly. It is highly unlikely that a judicial officer will rely on the testimony of the owner of a business whose only basis for forming an opinion of the business value is that of an owner.

What Do I Need To Disclose To My Spouse About The Business During The Divorce?

The owner of a business must provide the other spouse with all relevant material facts and information about the business. There is some question as to exactly what that means. Rather than ask what I need to disclose, the better and safer question is what do I not need to disclose? To avoid a potential set aside of the judgment or settlement after the matter is settled, the owner should over disclose. What does this mean? The owner should provide the other side with every relevant document and fact that relates to the value of the business. Some people explain the issue by saying that the owner should provide the other spouse with everything that a party would want to know, if they were considering buying the business. The family law attorney will not know what your should disclose unless you share the issues with that person.

Do I Need To Voluntarily Produce Records Or Wait Until I Am Asked To Produce The Records?

Yes, the law is clear that the owner of the business must voluntarily produce all relevant material facts and information to the other party. This may not be just documentation. It may include information that is not found in a document, like an oral offer to purchase the business.

What Are The Penalties For Failing To Disclose Important Facts About A Business?

Depending on the circumstances of the failure, the intentionality, motivation, or malice, the penalty may be 50% of 100% of the damages resulting from the failure to disclose, in addition to a substantial attorney fee award. The way to avoid this risk is over-disclose.

Do I Have To Disclose An Offer That I Received To Purchase The Business?

Yes. Any offer would be considered a material fact, even if made orally and even though not consummated. The contents, terms, price and identify of the potential buyer may be very relevant to the value of the business or facts related to it.

Do I Have To Disclose A Recent Appraisal Of The Business?

Yes. Clearly, an appraisal must be disclosed, even though the appraisal is not recent, was for a different purpose, used valuation methods that are not used in family law, and the facts and financial circumstances of the business are significantly different than they were when the appraisal was completed.

What Is A Final Declaration Of Disclosure?

The family code requires both parties to serve Preliminary Declaration of Disclosures on the other side. It also requires the parties to serve Final Declaration of Disclosure. However, while the preliminary disclosures cannot be waived, the final disclosures can be waived. However, while the service of the Final Declaration of Disclosure can be waived, the updated full disclosure of information cannot be waived. In other words, while a final disclosure can be waived, the content cannot be waived.

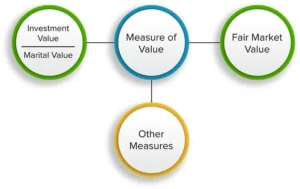

What Is The Investment Value Of A Business In A Divorce?

In a divorce context, businesses are not necessarily valued at fair market value. There are businesses that cannot be sold at a value that equals the true value of a business to the owner. A common misconception is that, in a divorce, a business lacks value if it heavily relies on the spouse operating it. The owner of a business may think that without that person, the business would not exist and that may be the case. However, in an Orange County divorce, businesses may be valued based on their “investment value” — the theoretical worth to the owner as the ongoing business — not necessarily what a third party would pay for the business. This approach recognizes the business’s intrinsic value, including the effort and resources the owner has invested.

How Are Taxes Considered In A Business Valuation?

California family law cases are clear, the courts cannot discount the value of a house, stock or a business relative to income tax unless the taxes are immediate, specific and arising out of the divorce. The court cannot speculate as to the amount of potential future taxes that may or may not be paid. The value of a business is not reduced even though it is clear that if the business was sold, there would be a substantial capital gains tax because the tax basis of the business is close to zero. Additionally, if the party being awarded the business is required to pay the other party a payment, known as an equalization payment, to equalize the overall distribution of assets, the payment is not tax deductible and is paid with after tax dollars.

What Date Is Used When Valuing A Business Valuation?

A business is usually valued at the date closest to the date of trial (or settlement) that is practical unless the court authorizes an alternate date. An alternate date could result from external factors that significantly impacted the value of the business or because the business is essentially a job for the operator. If the profit of the business is primarily a result of the work of one party, the business might be valued on the date of separation because that spouse’s post date of separation efforts, work and compensation are separate property and any increase in value after the date of separation would be a result of the separate property work of the operating spouse.

Who Is Awarded A Community Business?

Generally, a community business is awarded to the operating spouse. It is rarely ordered sold and if both spouses are critical to the business in different ways, the court will determine which person has the best prospects to operate the business in a success manner in future years.

How Do I Buy My Spouse’s Interest In A Community Business?

It is rare for the parties to agree or the court to order that a business be jointly owned after the date of the judgment. If parties have elected to be divorced, it is rare the working together is a logical solution. If a party is awarded the business, the value of the business will be placed on their side of the balance sheet at the value of the business as determined by the court and assets, if they exist in sufficient amounts, will be placed on the other spouse’s side of the balance sheet to offset the business value. If necessary, the spouse who was awarded the business may owe the other party an amount sufficient to equalize the assets awarded to the parties. In other words, if the wife is awarded the business at $400,000 and the husband is awarded the house at an equity amount of $200,000, the wife would have to pay the husband an equalization payment of $100,000 to that each party would have net assets of $300,000. The payment would bear interest if paid over time and would likely be paid over the next one to four years, depending on the financial practicalities.

How Does The Award Of The Ownership of A Business to One Spouse Affect Spousal Support?

The spouse awarded the business, will presumably earn an income from the business from which they will pay support. In other words, the value of the business to the ‘buying’ spouse is less than it would be in a non-divorce context, because the value of the business is, essentially, the income that it generates and a part of that income will be paid to the other party, who will also be paid for 50% of the value of the business. This is often viewed as a double dip and has been reviewed and approved by the appellate courts are equitable. Of course, if the business were sold, and both parties had other jobs, support would be paid in an amount related to the incomes earned by the parties.

How Is The Business Owner’s Income Determined For Purposes of Paying Support?

Income, in the context of paying support in a divorce, is often referred to as ‘ controllable cashflow available for the payment of support. This term of art is designed to include either income or distributions from a business as determined by the court. It also includes the personal expenses, referred to as ‘perks,’ paid by the business. It may also include funds left in the business that could have been distributed to the owner, without adversely impacting the cash flow needs or working capital needs of the business. Generally, voluntary (not mandatory) contributions to a retirement plan are added back to compensation and controllable cashflow. Depending on the nature of the depreciation, it may also be added back to controllable cashflow.

Can A Prenuptial Agreement Protect The Business During A Divorce?

Yes. The parties are free to execute a Prenuptial Agreement prior to the date of marriage that contains provisions that alter the rules that will be followed relative to the business if a divorce occurs in the future. In effect, the parties may replace California law with their chosen set of rules relative to business issues. These agreements can provide for such things as preventing the community from having any right to reimbursement relative to an increase in value of the business during the marriage or relative to any under-compensation to the operating spouse during the marriage. These agreements may also provide that all income and earnings of the business are the separate property of the owning spouse.

Can A Buy Sell Agreement, Signed After the Date of Marriage, Protect The Business From The Non-Operating Spouse?

A Buy Sell Agreement signed by the parties relative to a community property business, generally does not impact the parties’ rights in a divorce. It may be binding as to the parties and other business partners or shareholders but, the spouses generally don’t each have independent counsel and have not been informed as to the impact of the agreement on the parties in the event of a divorce.

How Are Accounts Receivable Considered In A Divorce Business Valuation?

Accounts Receivable are part of the book value of a business. Generally, an effort is made to determine which ones are collectable versus not collectable. This issue can be disputed if the write off of the accounts receivable is made during the pendency of a divorce. Although this is a gray area, it is generally thought that the accounts receivable should be valued on an after-tax basis in that, in the same way as deferred compensation and stock options, they are of no value until received and when they are received a tax is paid.

How Does The Court Determine The Character Of A Business, Community Property Or Separate Property?

Generally, the characterization of an asset, including a business is determined by the date of acquisition. This presumption can be overcome in certain circumstances depending on issues like source of funds used to acquire the asset and title to the asset.

How Can The Community Be Awarded A Part Of The Ownership Of The Separate Property Business Of The Other Spouse?

The community cannot acquire an interest in the ownership of a business during the term of the marriage unless the owner spouse signs an agreement that is a clear and express declaration of a change in ownership of that asset. If a business increases in value during the marriage, the community may acquire a right to financial reimbursement but not an ownership interest.

Conclusion

Divorces involving a business require careful analysis, strategizing and thought. By understanding the court’s approach to asset division, recognizing the unique challenges of valuing a business, and exploring strategic solutions, you can safeguard your financial interests during this difficult time. Whether through mediation or consultation with specialists, taking proactive steps can help manage the risks and complexities of divorce and business ownership in an Orange County divorce.

A Thorough Examination Of Separate Property In California Divorce

The division of property in a California divorce can be a complex and delicate matter. One of the most essential factors in this process is determining what constitutes separate property versus community property. Understanding these distinctions is vital, as it directly influences how assets are distributed between the spouses. This article delves into the specifics of separate property, how it interacts with community property, and the legal mechanisms that govern asset division in California.

What Is Separate Property?

In California, separate property is defined as property or assets that are exclusively owned by one spouse. This can occur under three main circumstances:

- Property acquired prior to marriage: Any assets a spouse owned before the marriage are typically classified as separate property.

- Gifts or inheritances: Any property received by one spouse as a gift or inheritance, regardless of when it was received, is considered separate property.

- Post-separation acquisitions: After the spouses legally separate, any property acquired by either party is classified as separate property.

The timing and method of acquisition are critical factors in determining whether property is classified as separate or community. Community property, on the other hand, refers to assets and income accumulated by either spouse during the marriage. In the event of a divorce, the law mandates an equal division of community property. However, this does not mean that each asset is divided equally. Instead, the court ensures that the overall value of the community property is split equally between the spouses, sometimes through the use of equalization payments to balance out the asset allocation.

Gifts And Inheritances: Retaining Separate Property Status

Under California law, gifts and inheritances remain the separate property of the receiving spouse, even if acquired during the marriage. However, the recipient must take care to ensure these assets are not commingled with community property.

For example, if inherited funds are deposited into a joint account shared with the other spouse, this mixing of assets may lead to the inheritance being treated as community property. To safeguard their status as separate property, gifts and inheritances should be kept in dedicated, separate accounts to avoid any unintentional blending with community funds.

Separate Property Businesses: Complexities In Classification

When one spouse owns a business before entering the marriage, that business is generally considered their separate property. However, if the business increases in value during the marriage—especially due to the owner-spouse’s efforts—the community may be entitled to a portion of that appreciation.

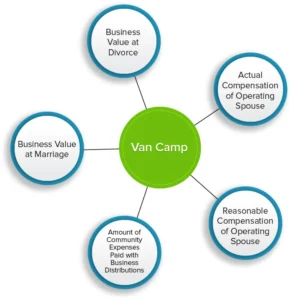

California courts rely on two key methods to determine the community’s share of a business’s growth:

- Van Camp Method: This approach is used when the business’s increase in value is mainly attributed to external factors, such as capital investment or market conditions, rather than the owner-spouse’s personal efforts. In this case, the community is typically compensated based on the reasonable value of the owner-spouse’s labor during the marriage.

- Pereira Method: This method is applied when the business’s success is primarily driven by the owner-spouse’s work, skill, and effort. Under this formula, the community is entitled to a portion of the business’s increased value, after allowing for a reasonable return on the owner’s separate property interest.

In rare cases, courts may decide to apply both methods at different stages of the marriage if the business undergoes significant changes over time. It is important to note that the non-owner spouse does not gain any ownership stake in the business itself; rather, they are entitled to financial reimbursement based on the business’s growth attributable to the community.

Valuing A Business During Divorce

If a business is started or purchased during the marriage, it is typically deemed community property. In such cases, the court generally awards the business to the spouse most actively involved in its operations. However, determining the value of the business is a critical step, often requiring expert testimony from financial professionals, such as forensic accountants.

California courts use two main valuation methods:

- Capitalization of Earnings: This method estimates the value of the business by calculating its future earning potential based on current earnings.

- Capitalization of Excess Earnings: This approach assesses the value of the business by analyzing its assets and determining the return generated on those assets.

These methods aim to determine the investment value of the business for the spouse who retains it, rather than focusing on what the business might sell for on the open market. If an equalization payment is required to ensure a fair division of property, it is calculated after taxes, and the payment is not deductible for the spouse making it.

Homes Owned Before Marriage: Applying The Moore Marsden Formula

When a spouse owns a home prior to the marriage, that property is classified as separate property. However, if community funds—such as income earned during the marriage—are used to pay the mortgage or improve the property, the community may gain a partial interest in the home’s increased value.

To calculate the community’s share of the property, courts apply the Moore Marsden formula. This calculation takes into account both the amount of mortgage principal paid with community funds and the appreciation of the property during the marriage. The non-owner spouse may be entitled to a portion of the home’s appreciation proportional to the community’s contributions.

If the owner-spouse wishes to convert the home from separate to community property, this must be done through a formal transmutation agreement, which clearly expresses the intent to change ownership. California law does not recognize informal promises or verbal agreements for transmuting property; a written agreement is required.

The Critical Role Of The Date Of Separation

In California divorces, the date of separation is a crucial legal milestone, as it determines when the accumulation of community property ceases. Any assets acquired after this date are classified as separate property.

For the separation to be legally recognized, one spouse must clearly communicate, through either words or actions, that the marriage has ended. A trial separation or merely living apart is insufficient unless accompanied by a clear intention to permanently end the marital relationship.

Proper documentation of the date of separation—through a written notice, email, or formal communication—can help avoid future disputes. This date is important as it influences how assets are divided, the duration and amount of spousal support, and the responsibility for debts incurred after the separation.

Post-Separation Financial Management: Handling Community And Separate Expenses

After the date of separation is established, each spouse’s earnings become separate property. However, complications may arise if one spouse uses their post-separation earnings to cover community expenses, such as mortgage payments or joint debts. In such situations, the paying spouse may be entitled to reimbursement, unless the payment directly benefits them (such as paying for a car they continue to use).

To avoid potential conflicts, it is advisable for separating spouses to separate their finances as soon as possible. This includes closing joint accounts, stopping the use of shared credit cards, and setting clear boundaries regarding financial obligations.

Practical Considerations For Protecting Financial Interests During Separation

To protect your financial well-being during a separation, it is essential to take proactive steps:

- Open a new, individual bank account for your earnings.

- Close all joint accounts and establish separate credit cards in your name.

- Update passwords for all personal and financial accounts.

- If you share a phone plan, consider switching to a separate provider.

- Set up a new email address specifically for communication with your attorney.

- Refrain from posting on social media until the divorce process is finalized.

- Seek advice from a divorce attorney before making any major financial decisions, such as investments or significant purchases.

Consult With An Irvine Divorce Lawyer

Our divorce lawyers at Minyard Morris are available for confidential initial consultations. If you live in Irvine and are ready to move forward with your separation or divorce, contact us today by sending us an inquiry or by calling our office at (949) 724-1111.