Why Minyard Morris Is the Right Fit for Your Divorce?

When You are navigating a divorce, especially one involving a business, choosing the ‘right’ lawyer is crucial. Look closely at what law firms say, and what they don’t say. Do their priorities match yours? Do they understand how they want their divorce handled? Carefully read their website.

Divorce is tough enough on its own, but when you add business interests or significant assets, the challenges multiply. The decisions you make now will affect your financial future, and overall stability for years. That’s why it is vital to have an experienced Laguna Niguel divorce lawyer who knows both family law and the ins and outs of valuating and dividing business assets. The right team can make the process smoother and less overwhelming.

At Minyard Morris, we understand what’s at stake. We’ve spent over 48 years helping clients in Orange County handle even the most complicated and high-stakes divorces. With 20 skilled divorce attorneys and more than 350 years of combined legal experience, we focus exclusively on family law. Our approach is personalized, strategic, and designed to get results. Our Laguna Niguel clients get the support and expertise they need to move forward confidently.

In 2024, the esteemed and independent lawyer rating service, Best Lawyers in America® listed 19 of 20 Minyard Morris family law attorneys.

Divorce For Business Owners: What Makes It Different?

Divorces involving a small business come with unique challenges that require careful attention, such as:

- Valuing The Business : A small business isn’t like addressing the value and dividing a bank account or home. Courts look at things like goodwill, tangible assets, cash flow, countless other issues. Courts generally rely on forensic accountants for valuations.

- Splitting The Assets : California’s community property law requires an equal division of community property. For business owners, that will mean compensating a spouse for their share of the business, which isn’t generally easy.

- Financial Stress : Running a business is demanding, even without the strain of divorce. Add accounting fees, legal fees, and potential support obligations, and the pressure can feel overwhelming.

At Minyard Morris, We’ve handled these situations for almost five decades. Our job is to protect the businesses of our Laguna Niguel clients and safeguard their financial future. Our job is to guide you through every step of the process.

How Are We Different?

Strategic Excellence

One of the ways we stand out is through our approach to strategic planning. Every week, our team meets three times a week —on Mondays at 5:00pm, Tuesday at noon, and Thursday at noon — to dive deep into our Laguna Niguel cases. These aren’t just routine check-inns; they’re collaborative sessions where we:

- Develop strategies for unique challenges,

- Analyze recent case law and how it might apply to our current cases.

- Discuss the preferences of specific judges and, those of opposing counsel relative to our strategy sessions.

With over 350 years of combined legal experience around the table, these meetings ensure that other cases will benefit from the collective expertise of our entire team. It’s a level of collaboration that all of our Laguna Niguel clients’ other firms simply can’t match.

Focused Personalized Representation

We don’t use cookie-cutter solutions. Every Laguna Niguel case is different, especially when a business is involved, we take the time to learn the story, understand the goals, and craft a strategy that works for our client. Whether it’s negotiating a favorable settlement or preparing for litigation, you’ll have a team that ‘s as invested in your success as you are.

Understanding Business-Related Issues In An Orange County Divorce

Divorce is multifaceted and emotionally challenging experience, especially when a small business is part of the equation. For business owners going through a divorce in Orange County, it’s crucial to grasp how the courts address the valuation and division of business interests. Unlike straightforward assets, businesses introduce significant complexities to a divorce process. This article delves into these intricacies, offering guidance to help our Laguna Niguel residents navigate this journey, whether by working effectively with a divorce attorney or exploring other representation options.

A clear understanding of business valuation can enhance the role of our Laguna Niguel clients, in the process, making you a more effective partner for your divorce attorney and forensic accountant. Familiarity with the steps involved can streamline the process and reduce fees. Moreover, understanding how businesses are valued during the divorce can help you weigh the advantages and disadvantages of hiring a divorce lawyer and forensic accountant.

For many small business owners, the costs of retaining legal and financial experts can feel prohibitive. However, failing to engage these professionals can lead to costly mistakes, such as an inaccurate business valuation that dramatically affects the financial outcome of the divorce. For instance, investing $25,000 in a divorce lawyer might save you $150,000 if the court assigns a more favorable value to your business, yielding a sixfold return on the investment. Although no divorce attorney can promise such results, this scenario is meant to illustrate the potential value of professional assistance.

How Is Property Divided In An Orange County Divorce?

To understand the role of a business in property division, it’s essential to understand the broader principles. In Orange County divorces, the law requires an equal division of community property. This does not mean every asset is split equally but rather that each spouse receives one half of the total marital estate’s value. Determining the value of all community property, including business interests, is required in order to equally divide the assets.

For example, if a business is valued at $400,000 and the couple’s remaining assets total $100,000, the marital estate equals $500,000. Each spouse is entitled to $250,000. The spouse retaining the business would need to pay the other $150,000 to ensure an equal division. These payments may be structured over time due to liquidity issues and may involve considerations such as interest rates, payment terms, and security for the debt.

An alternative method, though unusual, is a “global settlement”, where both parties agree not to prepare precise asset valuations and accept an uneven split of the marital estate. This approach must originate from the clients, not their divorce attorneys, and if s party is receiving less than fifty percent of the community estate, the code requires a clear, informed waiver of community property rights.

Are There Any Unique Challenges In Valuing Small Businesses In An Orange County Divorce?

Valuing a small business during divorce presents distinct challenges. Unlike larger corporations, the value of a small business often hinges on intangible factors like the owner’s reputation or client relationships. Engaging an experienced divorce attorney and forensic accountant is advisable, as they can employ sophisticated methods to assess the business’s worth, taking into account goodwill, cash flow, equipment, liabilities, and other elements.

However, the cost of these experts can strain small business owners, particularly when the business generates just enough revenue to cover personal expenses. Additionally, small businesses often lack accurate or professionally maintained financial records, further complicating the valuation process.

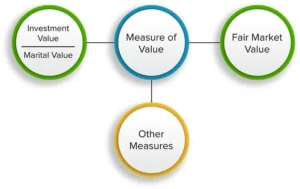

Because many small businesses are not readily sellable at economically feasible prices, courts typically use the “investment value” approach, valuing the business’s financial worth to the owner, rather than its fair market value. This perspective focuses on the economic benefit the business provides to its operator, avoiding speculative methods that project future earnings or rely on comparable sales.

What Methods Are Used By Family Law Courts In Divorces?

In Orange County, courts often rely on two primary methods to value businesses: the capitalization of excess earnings (an asset-based approach) and capitalization of earnings (an income-based approach). Methods involving projections of future earnings, such as the discounted cash flow method (DCF), are not permitted in family law, as they are considered speculative.

Courts also refrain from using industry-specific “rules of thumb”, which are general valuation shortcuts based on past transactions. These rules lack the evidentiary foundation needed in family law cases, as they do not account for critical details such as geographical differences, transaction terms, or financial details of all price sales that were used in developing the “rules”.

What Is “In-Place” Value?

When a business lacks actual goodwill as calculated by the formulas, the court may assign an “in-place” value, reflecting such things as location, phone numbers, website, and some customers. This value is typically lower than goodwill but acknowledges that the business has functional, tangible value as an ongoing concern.

Are There Any Common Misconceptions By Business Owners About Business Valuation In An Orange County Divorce?

Some business owners believe that if a business relies heavily on their efforts, that it has no value without them. Courts, however, are required to assign a value to all marital assets, including such businesses. Although the value may be limited, it is still part of the marital estate. Similarly, courts cannot force a spouse to sell or continue operating a business, though closing it without proper procedure can lead to claims of waste or breach of fiduciary duties.

Are There Any Alternative Representation Options In A Divorce?

While it’s possible to represent yourself in a divorce, doing so comes with significant risks, particularly if your spouse retains skilled professionals. Without expert evidence, the court may assign an unfavorable or incorrect business value. For those facing financial constraints, alternative options include:

- Mediation : This approach can be effective for resolving business valuation disputes without trial. A mediator can guide discussions and may recommend retaining a forensic accountant jointly.

- Unbundled Services : You can hire a divorce attorney for specific tasks, such as handling business-related issues, without full representation.

- Consultants : Engaging a newer, less experienced divorce attorney or forensic accountant as a consultant, can provide some guidance at a lower cost.

Should Business Owners Be Aware Of Any Special Considerations If They Are Facing A Divorce?

- Pre-Marriage Ownership : Businesses owned before marriage remain separate property. However, if the business increased in value during the marriage, the community may have a reimbursement claim.

- Support Payments : It may feel unfair to buy out your spouse’s interest in the business only to pay spousal support from its profits. However, California law permits this, and courts view it as distinct from the property division process.

- Retirement or Closure : Courts cannot compel a spouse aged 65 or older to continue operating a business. However, proper procedures must be followed to avoid claims of waste when closing or selling a business.

- Fiduciary Duties : Establishing a business competing with a community business, at a time when the community had sufficient funds to make the investment, while married could breach fiduciary obligations and lead to legal liabilities.

Can The Family Law Courts Consider Potential Future Speculative Events Relative To The Valuation Of A Small Business In A Divorce?

Courts generally value businesses as close to trial or settlement date as is possible. Businesses dependent on personal services may be valued as of the separation date. Future business profitability or potential threats are not considered in valuations, as courts focus on historical data, taxes are only factored in, only when they are immediate, specific, and arising out of the divorce.

Experiencing A Divorce In Laguna Niguel? Consult With A Divorce Attorney When You Are Ready

Selecting the right Laguna Niguel attorney for your divorce is critical. With over 600 divorce lawyers in Orange County, the process of choosing can feel overwhelming. At Minyard Morris, we stand out for our unwavering commitment to strategy, collaboration, and client success. For over 48 years, our firm has been a trusted name in family law, consistently delivering outstanding results.

If you have a small business and are getting a divorce, take the next step and call us at (949)724-1111. Or reach out via our online consultation form. Let us provide the guidance and representation you need to navigate your divorce with confidence.