Navigating a divorce is rarely straightforward, especially when complex assets or business interests are involved. The way these issues are managed during the divorce process can have a profound and lasting effect on your future—financially, emotionally, and personally. Ensuring that your rights and interests are fully protected requires the guidance of a skilled divorce attorney with the experience to handle the unique challenges posed by high-value assets and intricate financial details. The right legal representation can make a meaningful difference, allowing for a smoother, more equitable process and a successful outcome that meets your needs.

At Minyard Morris, we understand the importance of feeling supported and confident in your legal team, particularly in such a pivotal moment in life. Recognized nationally as a premier family law firm, we are known for our commitment to handling even the most complex divorce cases with professionalism, dedication, and compassion. Our team consists of 20 highly specialized divorce attorneys who exclusively focus on family law cases within Orange County, allowing us to bring deep, local expertise and insight to every case. With more than 350 years of combined experience, our attorneys are equipped to address even the most challenging issues with efficiency and care.

Our approach is client-centered, and we prioritize understanding each client’s unique circumstances. Our goal is to help you become a “former client” as smoothly as possible. We recognize that no one wants their divorce to extend any longer than necessary, and we are dedicated to helping our clients resolve their cases efficiently so they can confidently transition into the next chapter of their lives. With Minyard Morris, you have a team that works diligently and compassionately to guide you toward a favorable resolution, protecting your interests and providing peace of mind along the way.

Collaborative Strategy Meetings

These essential conferences occur every Monday at 5:00 pm, Tuesday at noon, and Thursday at noon. During these sessions, the attorneys address various critical aspects of pending cases, including:

- Strategies for engaging with opposing counsel

- Approaches to unique issues presented by assigned judicial officers

- Relevant case law and recent appellate court decisions

- Insights from new statutes and seminars

- Similar cases previously handled by the firm

- Settlement options and trial strategies

- Evidentiary considerations and likelihood of success

- Clients’ objectives and goals

Advantages For Clients

The value derived from these collaborative meetings is substantial, albeit challenging to quantify precisely. By harnessing the combined expertise of 19 family law attorneys specializing in Orange County cases, Minyard Morris provides clients with a notable advantage over smaller firms. Key benefits include:

- Swift access to pertinent case law and precedents

- Objective assessments of disputed issues

- Insights into the likelihood of success on specific matters

- Recommendations for expert consultations tailored to individual cases

- Innovative solutions for overcoming settlement obstacles

Commitment To Excellence

Minyard Morris allocates significant resources to these meetings, which are never billed to clients. The firm recognizes this practice as a vital differentiator in the family law landscape, underscoring its commitment to delivering exceptional client service and achieving optimal outcomes. This collaborative approach not only enhances the quality of legal representation but also attracts top-tier legal talent to the firm. It stands as a testament to Minyard Morris’s dedication to excellence and its unique position within the Orange County family law community.

Yorba Linda Family Law Attorney for Business Owners: Navigating Divorce with a Business at Stake

Divorce can be a complicated, emotionally taxing experience, and for those who own a business, it can become even more complex. When a business is involved in the marital assets, understanding how the courts assess its valuation and equitable division is essential. Unlike dividing simpler assets, the process of valuing and dividing a business introduces unique layers of complexity, requiring specialized knowledge and careful preparation. This article provides a comprehensive look into the process of dividing a business during divorce and offers essential guidance for business owners facing these challenges.

This article aims to help you work effectively with your family law attorney. By gaining a solid understanding of business valuation, you can become a more valuable partner to your Yorba Linda family law attorney and forensic accountant, ultimately making the divorce process more efficient and cost-effective.

Why It’s Essential To Retain Both A Family Law Attorney And A Forensic Accountant

Engaging a family law attorney and a forensic accountant might seem like a substantial financial commitment, but it’s essential to consider the potential cost of not hiring these experts. The crucial question is: what financial consequences could you face if you do not hire a lawyer and accountant to ensure an accurate business valuation? An incorrect valuation can result in significant financial losses. Investing in a qualified family law attorney in Orange County may turn out to be one of the wisest financial decisions you make, especially when you consider the difference between an accurate, professionally assessed business value and one left open to guesswork. Understanding these factors can help you collaborate with your professionals and, in the end, reduce overall costs.

Is An Expert Required For Business Valuation In Divorce?

Technically, a business owner can testify about their business’s value, but in most cases, this testimony may not carry much weight in court, especially if the opposing party has engaged a qualified valuation expert. Most business owners lack a detailed understanding of the legal principles involved in business valuation for family law cases, as well as the rules of evidence required in court. Without this knowledge, they may struggle to testify effectively, and important documents might be inadmissible.

A qualified valuation expert, by contrast, provides a well-founded opinion based on thorough research and analysis. Courts tend to value the credibility of experienced experts more than the subjective opinion of a business owner. A family law attorney can coordinate with a forensic expert, but they cannot provide a professional valuation opinion on their own. Without a forensic expert, the team required for a divorce case involving a business remains incomplete. The court will ultimately determine which party’s evidence of business value is more persuasive, and it is highly unlikely that a judge would rely on an owner’s valuation without expert analysis.

What Information Must You Disclose About The Business To Your Spouse?

As the business owner, you have a legal duty to provide your spouse with all pertinent information about the business. While it may be difficult to define exactly what qualifies as “relevant” information, a safer approach is to ask, “What would I want to know if I were the one asking for disclosure?” Over-disclosure is generally advised to avoid the risk of having your settlement or judgment overturned later. Over-disclosure means giving your spouse access to every document and fact that could affect the business’s valuation. Some professionals suggest that a business owner should provide their spouse with any information one would want to know before purchasing the business. Sharing full details with your family law attorney can also help them offer more effective guidance.

Should You Wait For Document Requests Or Voluntarily Disclose Records?

No, it is not sufficient to wait for your spouse to request records. California law mandates that a business owner must voluntarily disclose all significant information to the other party. This includes both documentation and verbal information, such as any oral offer made to purchase the business.

What Are The Consequences Of Failing To Disclose Essential Business Details?

Failing to disclose critical business information can lead to serious penalties. Depending on the circumstances, such as intent, motivation, or malice, penalties can include awarding the non-disclosing spouse 50% to 100% of the damages caused by the lack of disclosure, as well as potentially significant attorney fees. Avoiding these consequences is straightforward: full and proactive disclosure of all relevant information is essential to safeguard your interests.

Must You Disclose Offers Received To Purchase The Business?

Yes, any offer to buy the business, even if only verbal or ultimately unconsummated, qualifies as a material fact that must be disclosed. Information about the offer terms, price, and the potential buyer’s identity could significantly impact the business’s valuation.

Is Disclosure Necessary For A Recent Business Appraisal?

Yes, any recent business appraisal must be disclosed, regardless of why it was conducted, when it was done, or the methods used. Courts view past appraisals as highly relevant to the business’s value, irrespective of the purpose of the original assessment.

What Are Final Declarations Of Disclosure?

California Family Code requires both parties to submit a Preliminary Declaration of Disclosure, followed by a Final Declaration of Disclosure. Preliminary disclosures are mandatory and cannot be waived, while Final Disclosures may be waived if both parties agree. However, while the submission of the Final Declaration can be waived, the responsibility to provide fully updated financial information cannot be waived. In other words, the obligation to disclose up-to-date details remains even if the Final Declaration itself is waived.

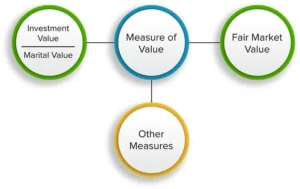

What Is The Investment Value Of A Business In Divorce?

In divorce, businesses are not always valued based on their fair market value. Many businesses may not be sellable at a price that reflects their true worth to the owner, yet they retain significant “investment value.” A common misconception is that a business has no value if it heavily relies on the spouse who operates it. While it’s true that some businesses depend on the owner’s involvement, Orange County courts often value a business based on its “investment value”—its worth to the owner as an ongoing entity, not its hypothetical sale price. This approach recognizes the time, resources, and effort that the owner has invested in the business, reflecting its intrinsic worth to them.

How Are Taxes Treated In Business Valuation?

California family law cases are clear that courts cannot discount the value of assets, including businesses, for potential income taxes unless these taxes are specific, immediate, and directly related to the divorce. Courts cannot speculate about future taxes. For example, a business’s value cannot be reduced based on anticipated capital gains tax, even if its tax basis is nearly zero. Additionally, if one spouse is required to make an equalization payment to the other to balance the division of assets, that payment is not tax-deductible and must be paid with after-tax dollars.

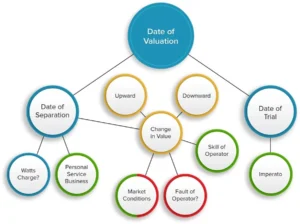

Which Date Is Used To Value A Business In Divorce?

Generally, a business is valued at a date as close as possible to the trial or settlement date, unless the court approves an alternate date. An alternative valuation date might be used if external events significantly affect the business’s value or if the business relies heavily on one spouse’s personal involvement. If the business’s earnings are mainly the result of one spouse’s labor, the valuation might be based on the date of separation, as any increase in value due to post-separation work is considered separate property.

Who Is Typically Awarded A Community Business?

In most cases, the court awards the community business to the spouse actively involved in its operation. Courts rarely order the sale of a community business. If both spouses play critical roles in the business, the court will assess which spouse is more likely to manage it effectively in the long term.

How Can You Buy Out Your Spouse’s Interest In A Community Business?

It is rare for the court or the parties to agree that a business should be jointly owned following the divorce. Since the couple has opted for separation, continued collaboration is often unfeasible. When one spouse is awarded the business, its assessed value is assigned to that spouse on the asset balance sheet, while other assets (if available) are allocated to the other spouse. If necessary, the spouse retaining the business may owe an equalization payment to the other. For example, if the wife is awarded a business valued at $400,000, and the husband receives $200,000 in home equity, the wife may need to pay the husband an additional $100,000 to ensure each spouse receives net assets of $300,000. This payment may include interest if made over time, typically within one to four years, depending on financial circumstances.

How Does Business Ownership Affect Spousal Support?

The spouse awarded the business is expected to earn income from it, which is then factored into spousal support calculations. In essence, the business’s value to the awarded spouse is lower in a divorce context, as its income stream may be used for spousal support. This concept, sometimes seen as “double-dipping,” has been upheld by appellate courts as a fair practice. If the business were sold and both spouses earned independent incomes, support would be calculated based on those incomes alone.

Determining The Business Owner’s Income For Support Payments

In divorce, a business owner’s income for support is often termed “controllable cash flow available for support.” This includes income or distributions from the business, along with personal expenses covered by the business, often called “perks.” It may also encompass retained earnings that could reasonably be distributed without negatively affecting the business’s cash flow or working capital. Voluntary retirement contributions are generally added back to controllable cash flow, as is depreciation when applicable.

Can A Prenuptial Agreement Safeguard The Business?

Yes, a prenuptial agreement made before marriage can alter the rules governing the business in a potential future divorce. Such agreements can provide that business-related income and any increase in business value during the marriage are separate property, protecting the owning spouse’s interests. A prenup can replace standard California law with the couple’s agreed-upon terms, giving greater control over the division of business-related assets in divorce.

Does A Buy-Sell Agreement Signed After Marriage Protect The Business?

Generally, a Buy-Sell Agreement signed after marriage does not alter each spouse’s rights in a divorce. While it may affect business relationships with other shareholders or partners, it typically doesn’t impact spousal rights without independent counsel and an understanding of how the agreement will affect a future divorce.

How Are Accounts Receivable Treated In Business Valuation?

Accounts receivable are considered part of a business’s book value. Typically, an effort is made to differentiate collectible receivables from non-collectible ones. This issue can become contentious if receivables are written off during the divorce proceedings. Generally, accounts receivable are valued after taxes, similar to deferred compensation or stock options, as their actual value is only realized when collected, at which point they are subject to tax.

Determining Whether A Business Is Community Or Separate Property

The characterization of a business as community or separate property usually depends on when it was acquired. A business acquired before marriage is generally separate property, although exceptions may apply depending on how the business was managed and funded. If the business increases in value during the marriage, the community may gain a right to financial reimbursement, though not an ownership stake.

Can The Community Gain An Interest In A Separate Property Business?

The community generally cannot acquire ownership in a separate property business unless the spouse who owns it formally changes the ownership. However, if the business’s value increases substantially during the marriage due to community effort, the non-owning spouse may be entitled to reimbursement for their contributions, even if they don’t gain a stake in the business.

Conclusion

Divorce cases that involve a business require careful preparation, analysis, and strategic planning. Understanding how courts handle asset division, recognizing the challenges of business valuation, and taking proactive steps to protect your interests are crucial. Whether through mediation or consultation with experts, taking a proactive approach can help you manage the risks and complexities of divorce and business ownership in Orange County. Working with experienced professionals will enable you to navigate this challenging time with greater confidence and clarity.

What Is Separate Property In A Divorce?

In divorce proceedings, separate property generally includes assets that one spouse acquired before the marriage, obtained individually after the marriage, or received during the marriage through a gift or inheritance. The timing and nature of acquisition play a significant role in determining whether an asset is separate or community property.

To elaborate, if an asset was acquired by one spouse prior to the date of marriage, it’s typically considered their separate property, as it wasn’t earned or purchased during the marital period. Additionally, assets obtained after the date of separation, which is the point at which one spouse has clearly communicated an end to the marital relationship, are also typically classified as separate property.

One common example of separate property is an inheritance. If a spouse receives an inheritance—whether before or during the marriage—it is considered that spouse’s separate property. However, it’s crucial that the inheriting spouse keeps the inheritance funds or property distinctly separate from marital finances to avoid commingling. Commingling occurs when separate and community funds are mixed together, making it difficult to distinguish separate property from community property. For instance, if an inheritance is deposited into a joint bank account shared with the other spouse, it could potentially lose its status as separate property, depending on how the funds are used.

The distinction between separate and community property is essential because, in a divorce, the court will identify and confirm each spouse’s separate property to remain with the respective owner. Meanwhile, community property is typically divided between the spouses, often on a 50-50 basis. However, this division doesn’t mean each item is split down the middle. The court has discretion in how it allocates assets to ensure each party receives an equal total value, rather than splitting every single item evenly.

Example: In a divorce, one spouse may be awarded a high-value asset, such as a car or a piece of artwork, while the other spouse may receive other assets or an equalization payment to make up for the difference in value. An equalization payment is a monetary amount paid by one spouse to the other to achieve a fair division of community property. However, this arrangement can sometimes create disputes regarding payment schedules, interest rates, or the total amount owed, adding another layer of complexity to the asset division process.

How Do Divorce Courts Handle Inheritances And Gifts?

In California, inheritances are generally classified as separate property belonging solely to the spouse who received the inheritance, irrespective of when it was acquired. This classification is critical because it means the other spouse has no legal claim to a share of the inherited asset. However, while the inheritance itself remains separate property, any income generated from it (such as interest or dividends) could potentially be factored in when calculating child or spousal support payments.

Similarly, gifts are viewed as the separate property of the spouse who received them, no matter when they were received. However, for an item to be legally recognized as a gift, certain requirements must be met. For example, to transfer ownership of a vehicle as a gift from one spouse to the other, a written statement must clearly indicate that the vehicle now belongs to the receiving spouse. Without this written document, the asset does not automatically become the receiving spouse’s separate property.

Example: Suppose one spouse gifts a car to the other for a birthday, wrapping it with a bow and celebrating the occasion. Without a formal written declaration of ownership transfer, the car may not legally be recognized as the receiving spouse’s separate property. This distinction ensures clarity on asset ownership and protects each party’s rights in the event of a divorce.

What Is Community Property In California?

In California, marital assets are categorized as either separate or community property. Community property typically includes assets and earnings acquired by either spouse from the date of marriage until the date of separation. This means that wages earned by either spouse during the marriage, as well as items purchased with those earnings, are generally considered community property, which will be subject to division in the event of a divorce.

However, this community property classification is a rebuttable presumption, meaning it can be challenged under certain circumstances. For example, if an asset acquired during the marriage was funded entirely by one spouse’s separate property—such as an inheritance or a gift—it may be deemed separate property. Additionally, if an asset is held in a title indicating sole ownership, this may serve as evidence that the asset was intended to be separate.

Example: Imagine a spouse receives an inheritance and uses those funds to buy a house during the marriage. Because the house was purchased using separate funds, it could be considered separate property, despite being acquired during the marriage.

How Are Earnings From Separate Property Treated?

Earnings generated from separate property generally retain their classification as separate property. For example, if a spouse owns a separate property stock that pays dividends, those dividends are considered separate property as well. The same principle applies to interest earned on a separate property bank account or rental income from a separate property home.

However, it’s crucial that these earnings remain separate from community funds to prevent commingling, which could affect their classification. For instance, depositing separate property dividends into a joint account could potentially convert them into community property.

Examples:

- Dividends paid from stocks owned as separate property remain classified as separate.

- Interest earned on funds in a separate account also retains its separate classification.

- Income distributed from a separately owned business stays with the owning spouse as separate property.

If these separate property funds are used to acquire a new asset, that new asset generally keeps its classification as separate property, as it derives from separate property funds.

How Is A Business Characterized In A Divorce Case?

A business that one spouse owned before the marriage is usually considered separate property. However, if the business’s value increases during the marriage, the community may be entitled to some form of reimbursement for the contributions that helped the business grow. This can happen if the owner-spouse actively worked in the business and directly contributed to its success, which benefits both spouses financially.

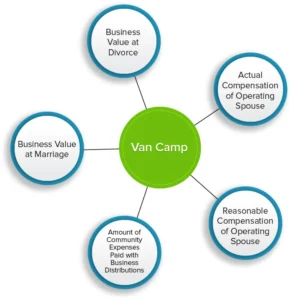

Courts typically use one of two primary formulas to calculate reimbursement:

- The Van Camp Method: This method is commonly applied when the business’s growth is mainly due to external factors, such as the capital investment or economic conditions, making it more suitable for capital-intensive businesses.

- The Periera Method: This Method is generally used in cases where the business’s growth is primarily due to the personal efforts of the owner-spouse, which is often the case in service-oriented businesses.

In some instances, the court may apply one method during one part of the marriage and the other method for another period, especially if the business’s nature changes significantly. Although rare, this split approach recognizes that a business can evolve, with different factors driving its growth at various stages.

Can The Community Acquire Ownership In A Separate Property Business?

No, neither the community nor the non-owning spouse gains an ownership interest in a business that’s classified as separate property. However, the community may have a right to reimbursement for any contributions made to the business during the marriage that led to its increased value.

Example: If the spouse who owns the business worked in it without fair compensation during the marriage, leading to an increase in the business’s value, the community may have a claim to part of that increase.

How Is A Business Valued In A Divorce?

For businesses established or acquired during the marriage, the court typically awards ownership to the spouse actively managing it, then calculates its value based on recognized valuation methods. Two of the most common methods are the capitalization of earnings approach, which considers the income the business generates, and the capitalization of excess earnings approach, which is more asset-focused.

It’s important to note that in divorce cases, courts are not permitted to speculate on the business’s potential future earnings. Unlike in other valuation scenarios, where projections of future cash flow might be considered, divorce valuations focus on the business’s current value.

Can A Separate Property Business Become Community Property?

A separate property business can only become community property if the owning spouse signs a formal agreement, known as a transmutation, explicitly changing the business from separate to community property. This agreement must be in writing and must clearly express the owner’s intent to make the business a community asset. Verbal statements, informal agreements, or casual promises are not enough to change a business’s classification in the eyes of the law.

Can The Community Acquire An Interest In A Separate Property Residence?

If one spouse owns a home before marriage, that property is generally considered their separate property. However, if community funds are used to make mortgage payments on that property during the marriage, the community may gain a pro-rata interest in the home. This means the community could have a stake in the property’s value based on the portion of the mortgage paid with community funds and any appreciation in the home’s value.

Example: Suppose the couple uses money from a joint bank account to pay down the mortgage on a separate property home. In this case, the community could have a right to a share of the increase in the property’s value due to the community’s contributions.

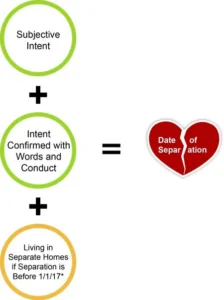

How Is The Date Of Separation Determined?

The date of separation is defined as the moment when one spouse clearly communicates their intent to end the marriage. This date is significant because it affects the classification of earnings, assets, and debts, as well as spousal support obligations. Establishing a clear date of separation can involve various actions, such as moving out, ending physical intimacy, or making a direct statement to the other spouse.

Selecting The Right Yorba Linda Family Law Firm Is Critical To The Success Of Your Family Law Matter

With over 600 divorce lawyers practicing in Orange County, the selection of the right lawyer may appear daunting. However, informed research and careful consideration will lead you to the most suitable lawyer for your situation.

When you need to consult with a family law attorney, call us at (949) 724-1111 or send us an email using our online Initial Consultation page. Let Minyard Morris be your partner through the complex world of family law, providing you with the expertise, support, and dedication you need to secure the best possible outcome for your case.