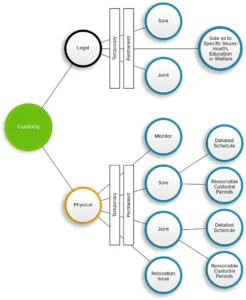

How Does Legal Custody Differ From Physical Custody?

Legal child custody addresses the right and responsibility to make decisions regarding a child’s health, education, and welfare. Parties are generally awarded joint legal child custody in Orange County Superior Court.

In unique situations, a family law court may award legal child custody to one parent in a designated area: education, extra-curricular activities, or medical issues. This type of child custody order may be made when the parties have a history of high conflict in one of these specific areas, and have demonstrated an inability to co-parent.

Most courts in Orange County are reluctant to make orders designating which school a child should attend, and courts will often award legal child custody to one parent on educational issues and authorize that parent to make the school selection decisions.

Physical child custody addresses where a child resides.

Parties may have joint or sole legal child custody and physical child custody.

Physical and Legal Custody

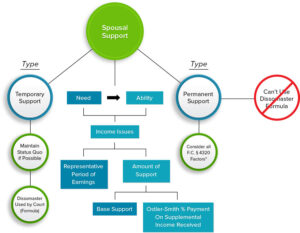

How Does Temporary Spousal Support Differ from Permanent Spousal Support?

It is not necessary to present evidence in the divorce trial to show a change of circumstances in order for the divorce court to have the ability to order a higher award of spousal support than it ordered for temporary spousal support (IRMO McNaughton). The family law courts look to different issues when determining permanent spousal support than when determining temporary spousal support. Temporary spousal support is designed to maintain the ‘status quo’ while permanent spousal support is based on the Family Code § 4320 factors.

The divorce court may not use the amount of temporary spousal support order as the basis for making a permanent spousal support order (IRMO Schulze).

Spousal Support

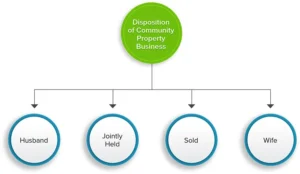

How is a Business Generally Disposed of in a Divorce?

It is rare that a business is sold as a result of the divorce. Unless there are very unique circumstances, a business is awarded to the operating-spouse. If the parties operate a business together and both seek an award of the business, it is generally awarded to the party that is most critical to its continued success. It would be rare for a divorce judge to award a business jointly to the parties. Continued joint ownership would most likely occur only if the parties were to agree.

On occasion, the operating-spouse of the business opposes having the business awarded to him. Rarely does a court order a business sold and even more rarely is a business awarded to the non-operating spouse. The operating-spouse often believes that there would be no business without him or her and he or she may be correct. However, to joint ownership in a divorce, that fact is not a determinative factor in the award of a business or the value of the business. Generally, the operating-spouse does not have the option to ‘shut down’ the business without the likelihood of being charged with the value of business as it existed before its closure.

A court may award a business to a party who opposes receiving the business as a part of his or her share of the community property (IRMO Rives).

Disposition of the Business

Initial Characterization of Business

How is Controllable Cash Flow Determined?

In family law matters, valuation experts render opinions as to the operating-spouse’s total controllable cash flow. Determining cash flow is not simply looking at the income or tax returns of the operating-spouse.

Income generally does not equal cash flow. A business may recognize significant income but have little or no cash flow in a particular year. On the other hand, a business may make substantial distributions in a year and have little or no income.

The amount of the controllable cash flow can be a significant source of conflict between the experts. Cash flow can be based on the income approach or the distribution approach. Cash flow generally includes the compensation of the operating-spouse, various perks and in certain situations the profits of the business. In divorces there can be an issue as to what portion of the profits could be distributed to the owner without adversely impacting the business operations which relates to the working capital needs of the business. Obviously, profits should not be added to cash flow if it would jeopardize the business’s ability to remain current on its debts and remain solvent.

Economic depreciation (vs. non-economic depreciation) should generally be added back to cash flow.

Compensation

How is Goodwill Calculated in a Family Law Matter?

In arriving at a goodwill value, the following factors, are considered: total compensation of operator-owner, reasonable compensation, rate of return on tangible assets, and multiplier/ capitalization rate.

Goodwill

How is Guideline Child Support Calculated? What is the “High-Earner” Exception?

Child support is calculated using a computer program (Dissomaster/X-Spouse), taking into consideration a number of factors including: the parent’s respective incomes, child custody timeshare, deductions, etc.

Divorce courts are required to find the amount of guideline child support. That sum will become the order of the divorce court, unless the court departs from the guideline child support, which the court can do for ‘good cause.’ Departures from guideline child support may be, but rarely are, ordered. A divorce court has the discretion to set child support below the guideline amount, if the payor-parent is found to be a ‘high-earner.’ If a finding of ‘high-earner’ status is made, then the divorce court must first determine the guideline child support level. After the guideline child support is determined, the divorce court is required to find whether it is the child’s best interest to receive child support below the guideline level of child support.

Child Support

Child Support

Only if the court finds that the guideline child support is unjust, will the court depart from the guideline child support and reduce the amount of the child support.

Generally, the amount of child support will increase if the payor-parent’s income increases. However, it will not necessarily increase to the guideline level, if the amount of the parent’s income results in a finding of ‘high-earner’ status. The divorce court has wide discretion determining whether a parent is a ‘high-earner,’ and as to whether to depart from guideline child support. The income level that justifies a ‘high-earner’ finding may differ from county to county, and from courtroom to courtroom, within the Orange County Superior Court.

A divorce court may also depart from guideline for other equitable or economic reasons, if it finds ‘good cause.’ ‘Good cause’ may be found when a child’s special needs are involved, when there are special education related issues, in situations where there was a deferred home award, where the recipient parent is not paying for their share of child expenses relative to that parent’s time share, travel expenses, and other circumstances where, without a departure from guideline the child support level, would create inequitable and unjust results.

Income Available for Support

An agreement to pay child support in excess of guideline child support is not modifiable downward to the guideline amount, unless the payor-spouse’s income decreases and such a decrease constitutes a material change in circumstances.

A change in the income of either parent, or in the custody timeshare between the parents, often results in a modification of child support.

The divorce court does not have jurisdiction to retroactively alter child support relative to a period prior to the filing of a request for modification of child support by a parent.

Time Share Factor

Income Factor

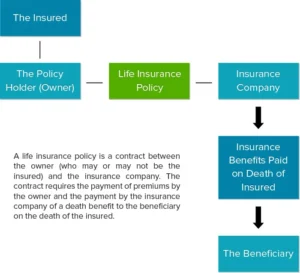

How is Life Insurance Valued in a Divorce?

Life insurance is an often overlooked asset in divorces. It may or may not be a significant issue but it most certainly should not be overlooked.

Life Insurance

How is Reasonable Compensation Determined?

There are two distinct approaches to determining the reasonable compensation of the operating-spouse. Differences of opinion in this area can lead to very significant differences in the values assigned to goodwill. One approach looks to the annual salary of a typical salaried employee who has similar experience to that of the owner-spouse. The other approach looks to the ‘similarly situated professional’ which is an approach that was addressed in the Orange County divorce case IRMO Ackerman. Using this approach, the divorce court looks at the cost of hiring a non-owner outsider to perform the exact duties as does the owner-spouse. This approach would assume that the individual had the same skill set, same contacts, same work ethic, etc. as the owner-operator. This approach generates a lower goodwill value than does the other approach.

Compensation

How is Spousal Support Generally Structured?

Spousal support may be structured in a variety of ways to address the needs and circumstances that exist at the time the order is made. Generally, the payments are paid monthly in equal amounts; however, they may be structured with two components: 1) monthly payments, based on the payor’s base income and 2) periodic support payments equal to a percentage of fluctuating or supplemental income that exceeds base income received periodically by the payor. The second component, called an “Ostler-Smith” order, may be appropriate where the payor’s income fluctuates.